Forex: EUR/USD Reaction to the Fed Decision

At 11:00 (GMT+2), data on GDP for Germany, France, and Italy for Q3 will be released, followed by business sentiment and unemployment figures for the euro area at 12:00 (GMT+2). Forecasts suggest that France’s economy will slow from 0.3% to 0.1%, Germany will likely post zero growth after –0.3%, while Italy’s GDP is expected to rise 0.1% after –0.1% quarter-over-quarter and 0.6% after 0.4% year-over-year. Overall, the eurozone’s seasonally adjusted GDP growth is projected to slow from 1.5% to 1.2% YoY, while quarterly growth is expected to improve by 0.1%. Growth in the region remains weak due to deteriorating global market conditions amid ongoing trade tensions.

Previously, the EU resolved trade disputes with the U.S., but the agreement didn’t prevent some tariff hikes. Businesses in France and Germany continue to face pressure from rising taxes and reduced subsidies. Economic and industrial growth is largely supported by increased defense spending linked to the Russia–Ukraine conflict, which cannot serve as a sustainable foundation for long-term recovery. The eurozone’s economic sentiment index is expected to edge up from 95.5 to 95.7 points in October, while the services confidence indicator may slip from 3.6 to 3.3 points, and unemployment is projected to remain stable at 6.3%.

At 15:15 (GMT+2), the European Central Bank (ECB) will publish the results of its monetary policy meeting. Analysts do not expect any changes, as the current interest rate near 2.15% aligns with prevailing price dynamics in the region.

The U.S. Fed meeting brought no surprises: the regulator cut the rate by 25 basis points to 4.00% and warned of persistent economic uncertainty hindering long-term planning. Markets anticipate another 25 bps cut in December.

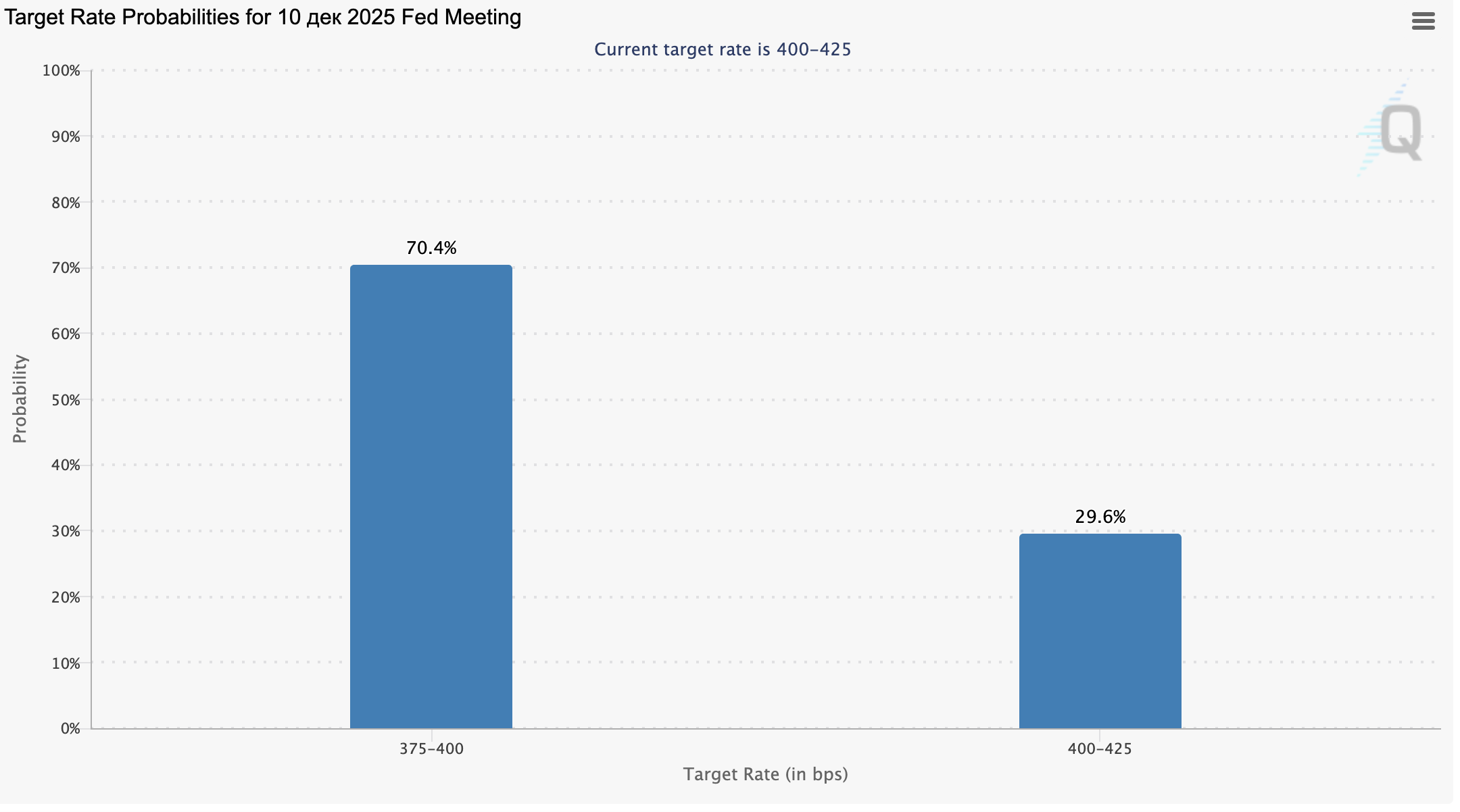

According to the CME FedWatch Tool, market participants estimate a 70.4% probability that the Fed will lower the rate on December 10, 2026, reducing the range from 4.00–4.25% to 3.75–4.00%. Only 29.6% expect the rate to remain unchanged, and 0% foresee an increase.

Thus, the market is almost certain that the U.S. Federal Reserve will shift toward a monetary easing cycle by the end of 2026.

GBP/USD

The pound shows mixed dynamics in the GBP/USD pair, hovering near 1.3160 as traders digest the Fed’s decision and await new market catalysts. On October 30, U.S. President Donald Trump met with Chinese President Xi Jinping. Previously, the White House announced 100% tariffs on Chinese imports starting November 1 in response to Beijing’s export restrictions on rare earth metals. Preliminary reports suggest the U.S. will drop these tariffs, while China delays its export curbs for at least a year. Both sides refrained from a joint statement, though Trump said he had reduced duties on Chinese goods by 20%. Meanwhile, traders continue to evaluate the Fed’s 25 bps rate cut to 4.00%.

The next Fed meeting will take place on December 9–10, and analysts expect another rate cut if inflation and labor conditions remain unchanged. In its accompanying statement, the Fed noted that economic activity continues to grow moderately, employment is slowing, and unemployment is rising but remains relatively low. The regulator is currently operating without full data coverage due to the ongoing U.S. government shutdown, which has delayed numerous economic reports. The Fed also confirmed plans to end quantitative tightening (QT) on December 1. In the UK, investors focused on consumer credit data showing net lending rising from £6.0 billion to £7.0 billion in September, surpassing forecasts of £5.5 billion, while mortgage approvals slipped slightly from 64,963 to 65,944 versus expectations of 64,500.

AUD/USD

The Australian dollar shows moderate growth in the AUD/USD pair, extending a short-term uptrend and testing the 0.6600 mark for an upward breakout. Support comes from optimism following the Trump–Xi trade talks at the APEC summit in South Korea, where the leaders discussed resolving the rare earth trade dispute. Trump described the meeting as “excellent,” noting several “outstanding” agreements, though no joint statement followed. He added that Beijing agreed to intensify anti-narcotics cooperation, while Washington halved tariffs on Chinese goods by 20%. Inflation data also strengthened the AUD, as quarterly CPI rose from 0.7% to 1.3% (forecast: 1.1%), and annual CPI increased from 2.1% to 3.2% (forecast: 3.0%). Core inflation climbed from 2.7% to 3.0% YoY and from 0.7% to 1.0% QoQ, exceeding expectations and reducing the likelihood of near-term policy easing by the Reserve Bank of Australia (RBA).

USD/JPY

The U.S. dollar is gaining moderately in the USD/JPY pair, testing the 152.85 resistance level as investors react to the Bank of Japan’s (BoJ) policy decision. As expected, the BoJ kept rates unchanged at 0.50%, with seven members voting for the hold and two (Takata Hajime and Tamura Naoki) favoring tightening amid rising inflationary pressure. Japan’s recent CPI data showed slight acceleration, staying above the 2.0% target. Officials are also likely mindful of Prime Minister Sanae Takaichi’s dovish stance and her plans to boost fiscal spending and restart stimulus programs.

Meanwhile, U.S. investors evaluated the Fed’s decision to cut rates to 4.00% while noting slow economic expansion. The prolonged government shutdown — now nearly a month — continues to disrupt official data releases as Congress remains gridlocked. On Friday at 01:50 (GMT+2), Japan will release industrial production and retail sales data for September, with forecasts indicating 1.5% growth in output after a 1.5% decline and retail sales rising 0.7% after –1.1%.

XAU/USD

The XAU/USD pair is rising, attempting to extend a short-term correction supported by the Fed’s policy decision. As expected, the regulator cut rates by 25 basis points to 4.00%. However, some FOMC members expressed differing opinions: Stephen Miran, appointed by the White House, favored a 50 bps cut, while Kansas City Fed President Jeffrey R. Schmid supported keeping the rate unchanged due to limited data. The U.S. continues to experience delayed macroeconomic releases amid the ongoing shutdown.

Democrats and Republicans have yet to reach an agreement, despite growing economic fallout. The Trump administration has warned of possible payment issues for military personnel starting mid-November, while many federal agencies are already furloughing non-essential workers. In addition to the rate cut, the Fed confirmed that quantitative tightening (QT) will end on December 1. Meanwhile, gold demand is pressured by optimism surrounding U.S.–China trade negotiations at the APEC summit in South Korea. Trump described the meeting as “great,” with several “notable” decisions made, though no joint communiqué followed. He also confirmed that Beijing agreed to increase anti-drug measures, while the U.S. halved tariffs on Chinese imports by 20%.