Forecasts suggest that Germany’s manufacturing PMI will edge up from 49.6 to 49.8 points, supported in part by higher defense spending, while the services PMI is expected to ease from 54.6 to 53.9. For the euro area as a whole, manufacturing activity is projected to rise from 50.0 to 50.2 points, with the services index holding at 53.0. At the same time, EUR/USD remains under pressure from expectations that the US Federal Reserve is unlikely to change monetary policy settings by year-end. Earlier, Fed Chair Jerome Powell warned markets against drawing quick conclusions about the December meeting, calling a rate cut “risky” given the lack of macroeconomic data during the government shutdown. Now that the federal government has resumed operations, investors can reassess the true state of the US economy.

Yesterday’s September labour market report showed that the US economy created 119.0K new non-farm jobs after a revised decline of 4.0K in the previous month (originally reported as a 22.0K increase), far above the 50.0K forecast. The unemployment rate ticked up from 4.3% to 4.4%. Average hourly earnings rose by 3.8% y/y versus expectations of 3.7%, while monthly growth slowed from 0.4% to 0.2% m/m (consensus 0.3%). Markets also noted the performance of existing home sales: in October, sales rose by 1.2% m/m after a 1.3% gain in September, with volumes increasing from 4.05M to 4.10M units versus a 4.08M forecast.

GBP/USD

The pound is strengthening against the US dollar in the GBP/USD pair, extending a fragile bullish impulse from the previous session. The pair is testing resistance at 1.3090, while investors are digesting US data released yesterday. The US currency gained fresh support after the September labour market report showed 119.0K new non-farm jobs versus a revised –4.0K in the prior month (from an initial 22.0K) and expectations of 50.0K. The unemployment rate rose from 4.3% to 4.4%, and average hourly earnings held at 3.8% y/y (consensus 3.7%), slowing from 0.4% to 0.2% m/m versus a 0.3% forecast.

This data set is unlikely to materially change the Fed’s rate decision at the 9–10 December meeting. In the UK, the focus today is on October retail sales, which disappointed: headline sales growth slowed from a revised 1.0% y/y (1.5% previously) to 0.2% y/y, while on a monthly basis the indicator fell from a revised 0.7% (0.5% previously) to –1.1% m/m, against forecasts of 1.5% and 0.0%, respectively. Ex-fuel sales came in at 1.2% y/y and –1.0% m/m after 1.7% and 0.7% previously, versus expectations of 2.5% and –0.2%. At 11:30 (GMT+2), November PMI data for the UK will be released: manufacturing activity is expected to soften from 49.7 to 49.3 points, and services from 52.3 to 52.1 points.

NZD/USD

The New Zealand dollar is gaining ground against the US dollar in the NZD/USD pair, holding near 0.5600 and the April lows. The main driver today is New Zealand’s October trade data: exports increased from 5.78bn NZD to 6.50bn NZD, while imports rose from 7.17bn NZD to 8.04bn NZD. As a result, the trade deficit narrowed slightly from –2.39bn NZD to –2.28bn NZD.

In the US, S&P Global will release November PMI data at 16:45 (GMT+2): the manufacturing index is expected to ease from 52.5 to 52.0 points, while the services index is seen steady at 54.8. Both readings remain above the 50.0 threshold, indicating that the economy still has a solid buffer, so a modest pullback is unlikely to significantly affect the Fed’s stance on further easing this year.

At 17:00 (GMT+2), updated inflation expectations from the University of Michigan will be published: analysts look for a one-year outlook at 4.7% and a five-year outlook at 3.6%. Traders also continue to assess the September labour market report released yesterday, which showed 119.0K new non-farm jobs versus an expected 50.0K, an uptick in the unemployment rate to 4.4%, and average hourly earnings growth of 0.2% m/m and 3.8% y/y.

USD/JPY

The US dollar is weakening against the yen in the USD/JPY pair, retreating from record January highs. The pair is testing support at 157.20 on a break lower as investors react to fresh inflation data. Japan’s national CPI rose from 2.9% to 3.0% y/y in October, while the core measure excluding food and energy climbed from 3.0% to 3.1%. This strengthens the case for further tightening by the Bank of Japan later this year, although the upside surprise is moderate and could be partly residual.

Export growth slowed from 4.2% to 3.6% y/y in October (consensus 1.1%), while imports decelerated from 3.0% to 0.7% y/y compared with expectations of –0.7%, leading to a slight narrowing of the trade deficit from –237.4bn JPY to –231.8bn JPY (forecast –280.0bn JPY). Business activity also improved: the Jibun Bank manufacturing PMI rose from 48.2 to 48.8 points, and the services PMI held at 53.1. In the US, yesterday’s September labour report showed 119.0K new non-farm jobs after a revised decline of 4.0K, with unemployment up to 4.4% and average hourly earnings at 3.8% y/y and 0.2% m/m.

Markets additionally tracked existing home sales data: in October, sales rose by 1.2% m/m after a 1.3% gain, with volumes up from 4.05M to 4.10M units, slightly above the 4.08M forecast.

XAU/USD

The XAU/USD pair is posting a modest decline in early trading, hovering near 4060.00. Gold looks set to finish the week roughly flat, with macro data from the US failing to provide a strong directional impulse. Yesterday’s delayed September labour market report, which had been postponed due to the government shutdown, showed that the US economy added 119.0K new non-farm jobs versus a revised –4.0K (from 22.0K) previously and expectations of 50.0K.

The unemployment rate rose from 4.3% to 4.4%, while average hourly earnings grew by 3.8% y/y (forecast 3.7%) and slowed from 0.4% to 0.2% m/m (consensus 0.3%). Existing home sales increased by 1.2% in October after a 1.3% rise in September, with annualised volumes climbing from 4.05M to 4.10M units versus 4.08M expected.

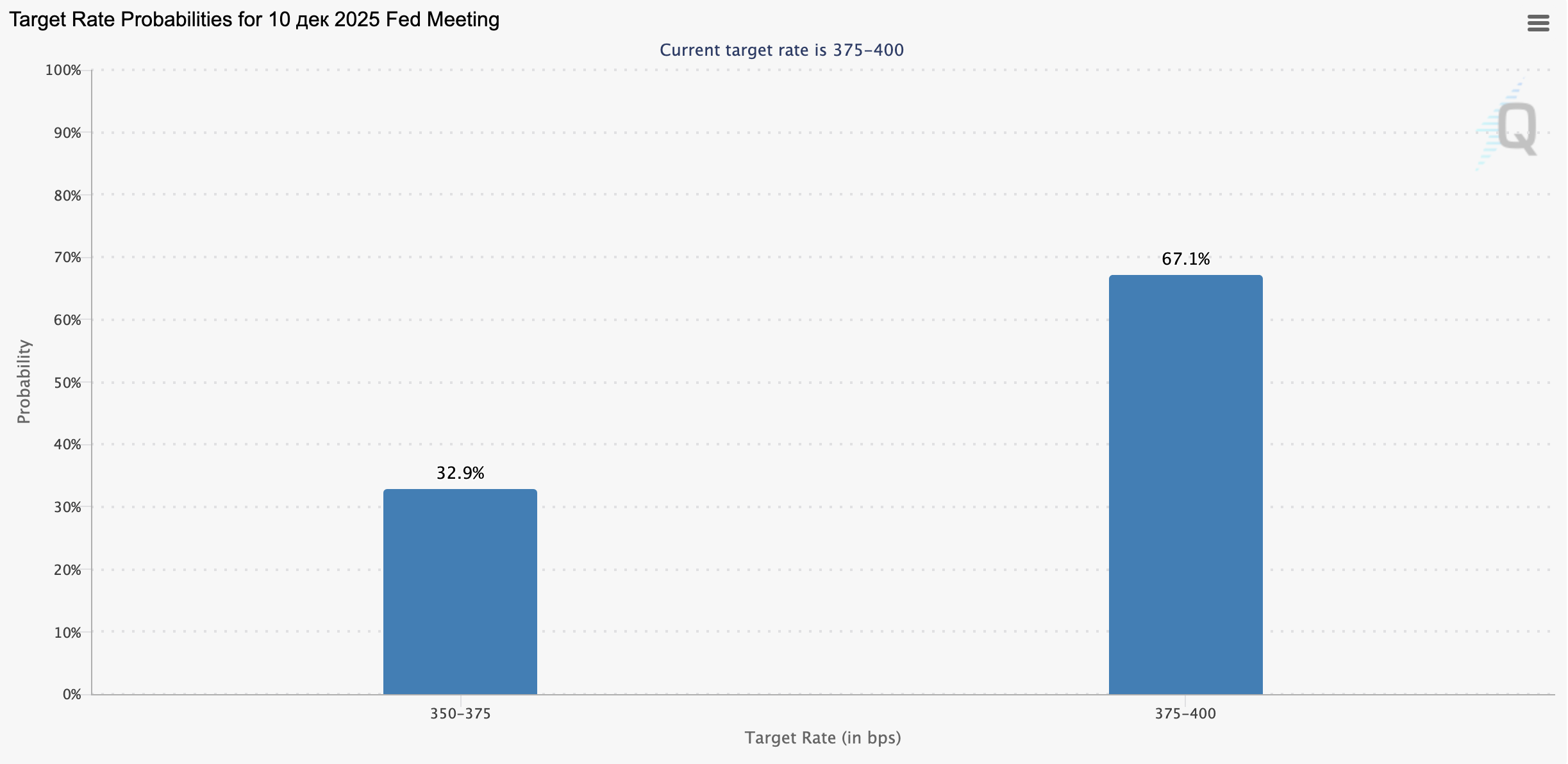

The US Department of Labor also announced it will not publish October employment data, citing the inability to collect a full set of statistics under current conditions. This shifts the spotlight to the November jobs report, due later than usual on 16 December. The lack of an October release will likely complicate the Fed’s December 9–10 rate decision, prompting markets to raise the odds that policymakers will prefer to keep monetary policy unchanged.