Forex Today: U.S. Dollar Dynamics and the Federal Reserve’s Policy Decisions

Investor attention in the forex market remains focused on the Federal Reserve’s latest monetary policy decision and the meeting between U.S. President Donald Trump and Chinese President Xi Jinping. Yesterday, the Federal Reserve reduced its interest rate to a target range of 3.75–4.00% and announced the end of its asset purchase reduction program, known as quantitative tightening, effective December 1. Ten members of the Federal Open Market Committee (FOMC) voted in favor of the move, while two opposed it. Board member Steven Miran advocated for a more aggressive 50-basis-point cut, whereas Kansas City Fed President Jeffrey R. Schmid suggested maintaining the current rate due to persistent inflationary pressures in the economy.

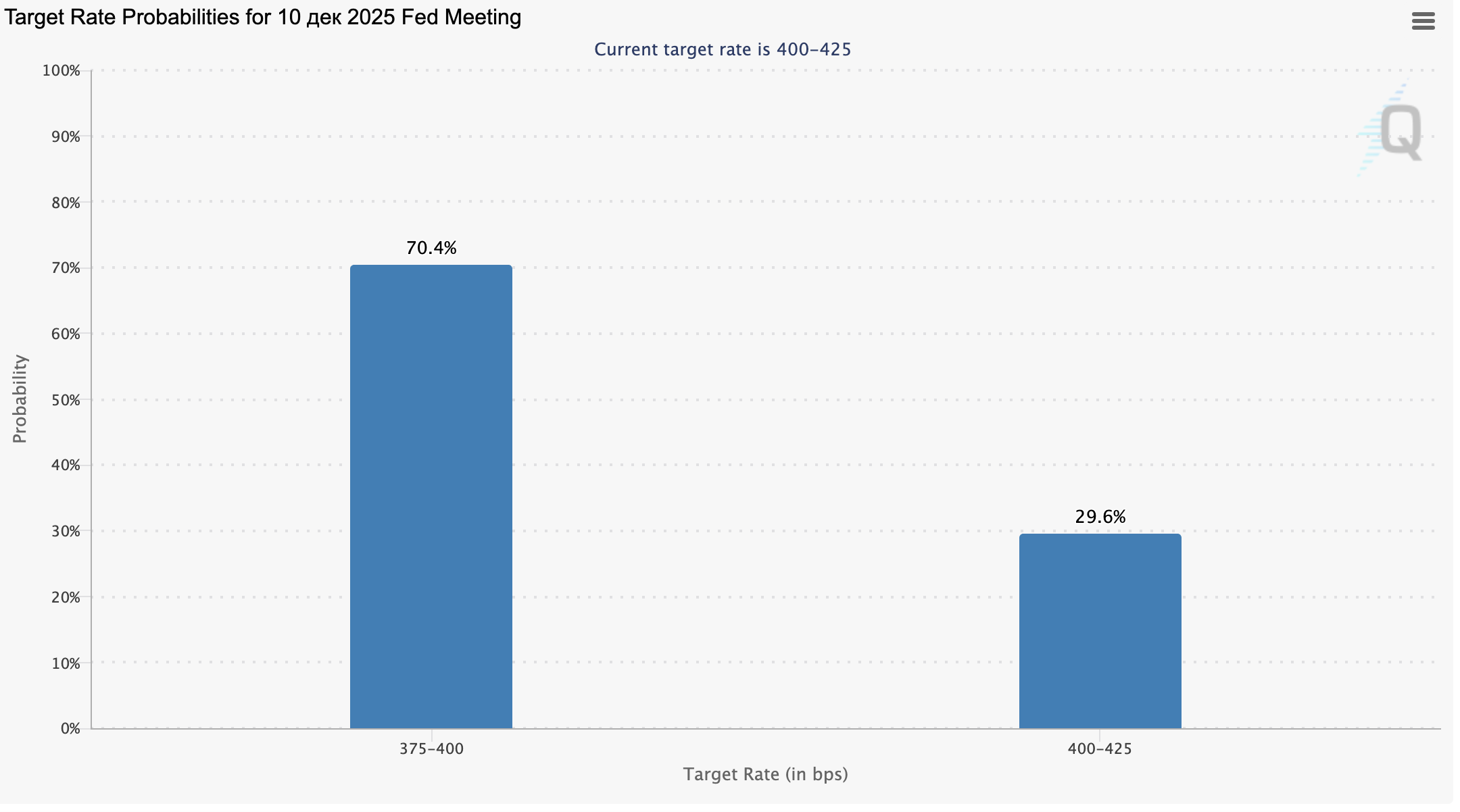

Following the meeting, Fed Chair Jerome Powell hinted that the regulator might pause in December to assess the impact of recent policy adjustments before proceeding with further easing. This cautious tone disappointed investors who had anticipated another rate cut by the end of the year. As a result, according to the CME Group’s FedWatch Tool, the probability of a December rate cut dropped from 90.0% to 67.0%.

Meanwhile, President Donald Trump announced that several trade issues with China have been resolved following his meeting with Xi Jinping. The U.S. confirmed that China will supply rare earth metals throughout the year, intensify efforts to combat fentanyl production, and increase imports of American agricultural goods. In exchange, Washington will reduce tariffs on Chinese exports by 10%, bringing the total tariff rate to 47%. Trump also revealed that he will visit China in April next year, followed by a reciprocal visit from President Xi to the United States.

Eurozone

The euro is weakening against the U.S. dollar but strengthening versus the pound and the yen.

Investors are focusing on the results of the European Central Bank’s (ECB) monetary policy meeting. As expected, the ECB kept all key interest rates unchanged — the main refinancing rate at 2.15%, the deposit rate at 2.00%, and the marginal lending rate at 2.40%. The regional economy continues to expand modestly, while inflation remains close to target levels: in September, headline inflation stood at 2.2% and the core rate at 2.4%. Under these conditions, most analysts expect the ECB to maintain its current stance until at least the end of the year.

Fresh preliminary data showed that the eurozone’s Q3 GDP rose by 0.2% quarter-over-quarter (versus the 0.1% forecast) and by 1.3% year-over-year (versus 1.2%). Spain’s GDP grew by 0.6%, France’s by 0.5%, both exceeding expectations of 0.2%, while Germany and Italy remained stagnant. Analysts believe the eurozone economy will sustain moderate growth into 2026, though significant downside risks remain amid weak external demand and high energy costs.

United Kingdom

The British pound is falling against the U.S. dollar and the euro but gaining slightly against the yen. Forex traders are preparing for the Bank of England’s upcoming policy meeting, scheduled for next Thursday at 14:00 (GMT+2). The majority of experts expect a 25-basis-point rate cut, following weak inflation data for September. The consumer price index (CPI) came in flat month-over-month and at 3.8% year-over-year, below the forecast of 4.0%. This reading may give the central bank room to ease policy further, with traders pricing a 75% probability of a rate cut in the near term.

However, policymakers remain divided. Some members of the Monetary Policy Committee continue to express concern about persistent price pressures, particularly in the services sector. At the same time, growing expectations of higher taxation under the new government budget may weigh on business activity and GDP growth prospects, keeping the pound under pressure in the medium term.

Japan

The Japanese yen continues to weaken against the euro, pound, and dollar.

As expected, the Bank of Japan left its key interest rate unchanged at 0.50%. Seven members of the Policy Board voted in favor of maintaining the rate, while two — Hajime Takata and Naoki Tamura — supported a 25-basis-point hike. In his press conference, BOJ Governor Kazuo Ueda said that the likelihood of tightening “has slightly increased,” but the central bank needs more macroeconomic data to determine whether companies will continue to raise wages despite the pressures from elevated U.S. tariffs. Analysts note that Japan’s monetary stance remains one of the most accommodative among major economies, though gradual normalization could begin in 2026 if inflation remains above target.

Australia

The Australian dollar is weakening against the euro, pound, and dollar but firming against the yen.

Today’s Q3 trade price data showed that export prices declined by 0.9% (compared with a 4.5% drop previously), while import prices fell by 0.4% (after a 0.8% decrease). Although the decline in prices is slowing, inflationary pressures remain high. The consumer price index rose 3.2% year-over-year in Q3, exceeding expectations of 3.0%. These figures may prompt the Reserve Bank of Australia (RBA) to maintain its current interest rate and delay any potential easing, thereby providing support to the Australian currency. The central bank’s cautious approach is consistent with its goal of returning inflation to the 2.0–3.0% target range over the medium term.

Oil

Crude oil prices are moving slightly lower following the Trump–Xi meeting results.

Analysts note that the newly reached agreements are likely to ease trade tensions rather than bring about structural change in relations between the world’s two largest economies. This means that risks of renewed trade disruptions and weaker energy demand remain. Nevertheless, further price declines are limited by the Federal Reserve’s recent policy easing — which pressures the dollar — and by a bullish report from the U.S. Energy Information Administration (EIA). The report showed a sharp 6.858-million-barrel drawdown in crude inventories (vs. a forecast of –0.9M), along with significant declines in gasoline (–5.941M) and distillate (–3.362M) stocks. These figures indicate robust demand in the U.S. and provide moderate support for oil prices, which continue to trade within a narrow range amid global uncertainty.