Forex: EUR/USD dynamics and the key drivers behind the rally

Later today at 12:00 (GMT+2), the eurozone will publish new GDP data. Forecasts suggest no changes from the previous reading, when the economy expanded by 0.2% quarter-over-quarter and 1.3% year-over-year. Labor market figures are also due, with expectations of 0.1% quarterly and 0.6% annual growth. Thursday’s eurozone data showed industrial production rising from 1.1% to 1.2% year-over-year in September, while the monthly reading improved from –1.1% to 0.2%, although still below the expected 0.7%.

The euro is also supported by growing expectations of monetary easing from the Federal Reserve, while the European Central Bank has almost fully wrapped up its own dovish cycle. Analysts believe the ECB may deliver just one more 25-basis-point cut in early 2026 at most.

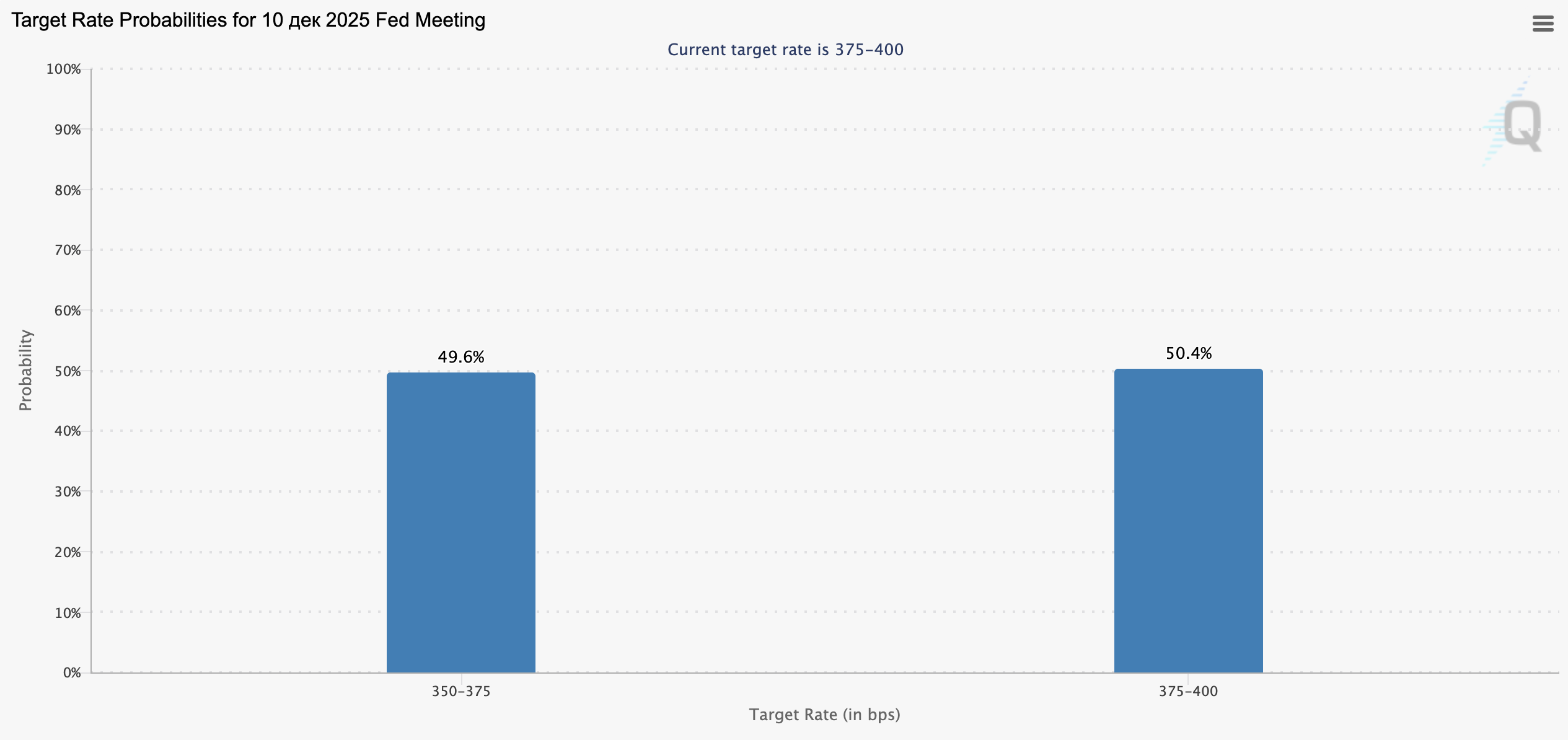

The chart reflects market expectations ahead of the Federal Reserve meeting on December 10, 2026. Traders are almost evenly split:

- 49.6% expect a rate cut to 3.50–3.75%

- 50.4% expect the Fed to hold at 3.75–4.00%

This distribution shows the market has no clear consensus. Investors and forex traders are waiting for fresh inflation and employment data before taking firm positions on the Fed’s next move.

The US central bank could still move forward with a December rate cut, and odds of such a decision have increased sharply since the end of the record-long US government shutdown. On Thursday, the House of Representatives voted 222 in favor of a temporary federal funding bill. Democrats secured several concessions from Republicans, although their key demand to reinstate healthcare subsidies was not met. Today’s US data on producer inflation and retail sales will be crucial: analysts expect PPI to remain at 2.6% year-over-year, while the monthly reading likely accelerates to 0.3% after –0.1% previously. A result in line with expectations would support the case for a pause in the Fed’s dovish cycle and offer moderate backing to the US dollar.

GBP/USD

The pound is losing ground against the US dollar, pulling back after yesterday’s bullish rebound, which had offset losses from earlier in the week. GBP/USD is now testing the 1.3140 level to the downside. Fresh UK macro data released yesterday showed a slowdown in Q3 GDP from 0.3% to 0.1% QoQ (vs. 0.2% expected) and from 1.4% to 1.3% YoY. The monthly reading dipped from 0.0% to –0.1%.

Industrial production data also disappointed: output fell 2.5% in September after –0.5% previously, versus expectations of –1.2%. Manufacturing activity contracted 1.7% MoM and 2.2% YoY, both weaker than forecasts. Earlier, the European Commission introduced steel and aluminum import tariffs above certain quotas — a move that will weigh heavily on the UK industrial sector, which sends up to 70% of its metal exports to the EU. Meanwhile, the US dollar remains under pressure as traders await a wave of delayed macroeconomic releases, likely reinforcing expectations of a December Fed rate cut. According to CME’s FedWatch Tool, around 55% of analysts expect Jerome Powell to opt for a 25-basis-point cut next month.

AUD/USD

The Australian dollar is trading mixed against the US dollar, though the pair is on track to finish the week with moderate gains. On Thursday, AUD/USD briefly reached new highs near 0.6580, but the move lost steam and sellers regained control by the session’s close. Strong labor market data provided solid support: employment jumped by 42.2K in October versus 12.8K previously and 20K expected. Full-time positions increased by 55.3K, while part-time employment dropped by 13.1K.

The participation rate held steady at 67.0%, while unemployment fell to 4.3% from a four-year high of 4.5%. Tasmania posted the lowest unemployment rate at 3.9%, followed by Western Australia at 4.1%. Inflation expectations from the Melbourne Institute fell from 4.8% to 4.5% in November, adding to the improving sentiment. A strong labor market and easing inflation may influence the Reserve Bank of Australia's next policy steps: the cash rate currently sits at 3.60%, unchanged since August’s 25-bp cut.

The RBA noted CPI rose 1.0% QoQ and 3.0% YoY in Q3, while the bank’s updated forecasts project a slowdown to 2.6% by 2027. Meanwhile, US markets await the first wave of macro releases since the government shutdown ended, including today’s retail sales report. Economists expect sales to slow from 0.6% to 0.4% MoM, with annual growth steady at 5.0%.

USD/JPY

The US dollar is showing mixed price action against the yen, consolidating near 154.50 and staying close to this year’s highs. The greenback remains under pressure following the shutdown, with traders preparing for a heavy flow of delayed US macro data — likely strengthening expectations of a Fed rate cut.

Today’s focus is on October producer inflation: the annual PPI reading is expected to remain at 2.6%, while the monthly figure should accelerate to 0.3% after –0.1%. Japan’s services activity index provided slight support for the yen, rising from 0.1% to 0.3%. Earlier, fresh PPI numbers showed annual producer inflation easing from 2.8% to 2.7%, while monthly growth slowed from 0.5% to 0.4%. Easing inflation pressures weaken the case for a more hawkish Bank of Japan — although the central bank still isn’t ruling out further rate hikes despite political pressure from the new prime minister.

XAU/USD

Gold is extending its weekly advance, with Thursday marking the only session of corrective pullback — largely technical in nature. The fundamental backdrop remains supportive: the US dollar continues to soften post-shutdown, and analysts expect upcoming macro data to reinforce dovish expectations for the Federal Reserve. At the moment, around 55% of analysts anticipate a 25-bp cut in December.

Markets also expect the Bank of England to consider easing as the UK economy shows growing signs of strain. Safe-haven interest in gold is additionally supported by geopolitical uncertainty tied to US trade and foreign policy. On Friday, Washington announced the launch of Operation “Southern Spear” in the Western Hemisphere — a development that could dampen risk appetite if tensions rise. Today, traders will be watching US retail sales and producer inflation data: retail sales are expected to slow from 0.6% to 0.4% MoM, with annual growth steady at 5.0%, while PPI should remain unchanged at 2.6%, and core PPI at 2.8%.