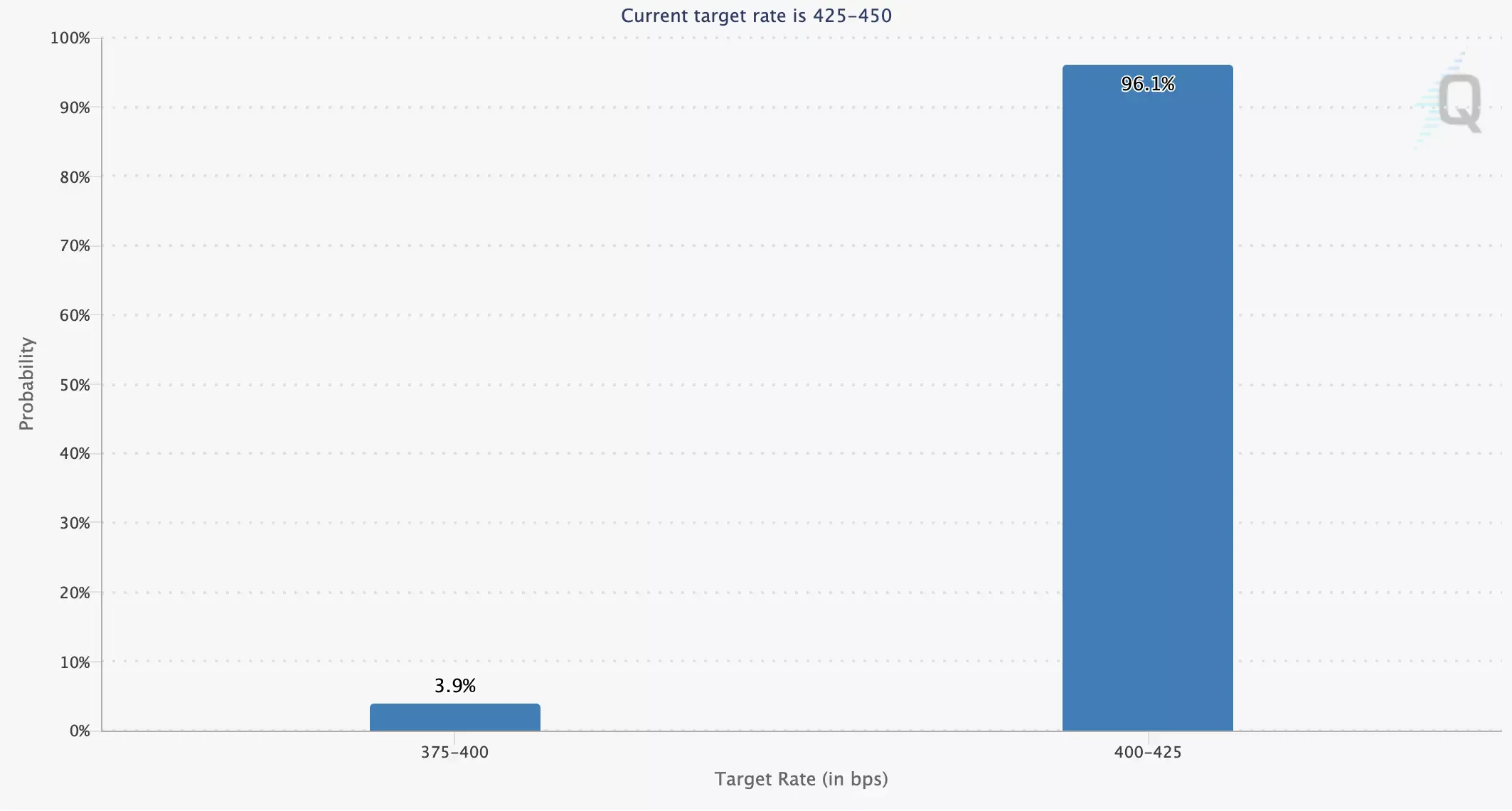

Although markets have already priced in a minimal rate cut at the upcoming Federal Reserve meeting, the results of which will be announced tomorrow at 20:00 (GMT+2), subsequent comments from Fed Chair Jerome Powell may act as a catalyst for stronger negative dynamics.

Investors and Forex traders expect signals of further monetary policy easing, but if Powell remains traditionally cautious in his remarks, pressure on him from President Donald Trump’s administration will increase. Market participants may then shift towards safe-haven assets such as gold, or move capital into cryptocurrencies. Analysts expect the Fed to announce at least two more rate cuts before the end of the year. In addition, tomorrow at 14:30 (GMT+2) housing market data will be released: housing starts in August are expected to decline from 1.428M to 1.360M, which also weighs against dollar growth.

Eurozone

The euro is gaining against the dollar, pound, and yen.

Published macroeconomic data indicates that the eurozone economy remains relatively stable despite tariff restrictions imposed by the US last month. Industrial production in July rose by 0.3% after –0.6% in the previous month (forecast 0.4%), while the annual growth rate accelerated from 0.7% to 1.8% (vs. forecast 1.7%). Meanwhile, wages in Q2 increased by 3.7% after 3.5% previously, and the labor cost index rose by 3.6%, exceeding expectations of 3.4%.

United Kingdom

The pound is strengthening against the dollar and yen but weakening against the euro.

Today’s labor market data showed that average wages in July adjusted to 4.8%, down from 5.0% in June, while total pay including bonuses stood at 4.7% versus 4.6%. Stable wage indexation boosted employment to 232K compared to preliminary estimates of 220K, following 238K in the previous month. As a result, the unemployment rate remained at 4.7% for the third consecutive month, after holding at 4.4% earlier this year.

Japan

The yen is losing ground against the pound and euro but strengthening against the dollar.

Investors are analyzing the trade agreement with the US, under which Japan must allocate $550B into the US economy via equity, loans, and guarantees within 45 days after Washington selects the investment target. Concerns arise over Tokyo’s ability to raise such funds amid higher-than-expected inflation and production levels comparable to those seen during the COVID-19 pandemic. Tomorrow at 01:50 (GMT+2) August foreign trade data will be released, expected to show an increase in the trade balance deficit to –513.6B yen, repeating May’s low.

Australia

The Australian dollar is strengthening against the US dollar but weakening against the yen, pound, and euro.

Deputy Governor of the Reserve Bank of Australia (RBA) Andrew Hauser noted that in the coming years Australian pension funds, which already allocate a significant portion of their portfolios abroad, will likely increase currency hedging on such investments. According to him, the Australian dollar serves as a “natural hedge”: when global risk assets decline in value, the national currency also weakens, partially offsetting funds’ foreign exchange losses. Currently, currency hedging covers about one-fifth of overseas equity investments.

Oil

Oil prices are trading near the key monthly level of 67.00.

Today, the International Energy Agency (IEA) released a report assessing investment prospects in oil and gas fields. Hydrocarbon production at existing sites continues to slow as current funding is sufficient only to cover ongoing development costs. This is mainly due to the high expense of deepwater exploration: since 2019, nearly 90% of annual financing has been allocated to offset production decline rather than meet demand growth. According to the IEA, oil and gas industry investments in 2025 will total about $570B compared to $599B in 2024.