Forex Analysis: EUR/USD Weakens Ahead of Eurozone Inflation Data

Forecasts suggest that the eurozone’s core consumer price index (CPI) will slow from 2.4% to 2.3% in October, while the broader index may decline from 2.2% to 2.1%. However, these numbers are of secondary importance, as the European Central Bank (ECB) is already nearing the end of its rate-cutting cycle. Analysts expect at most one more 25-basis-point reduction before year-end. Yesterday, the ECB again left the main refinancing rate unchanged at 2.15% and the deposit rate at 2.00%.

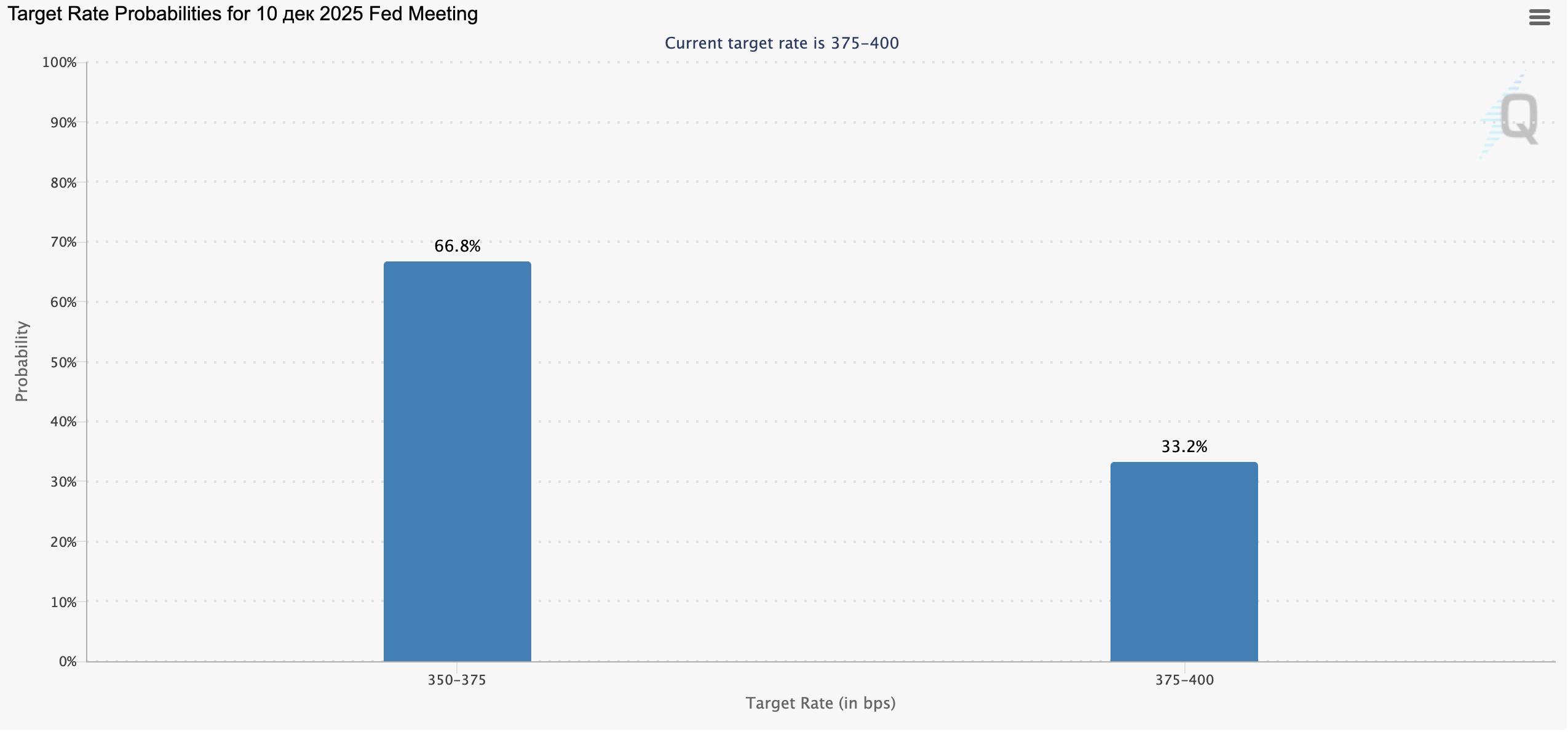

According to the CME FedWatch Tool, the probabilities for the December 10, 2025 FOMC meeting show a 66.8% chance of a rate cut to 3.50–3.75% and a 33.2% chance of maintaining 3.75–4.00%.

In its accompanying statement, the ECB reiterated that inflation remains close to the 2.0% target and that medium- and long-term expectations are stable. Officials also noted steady regional growth, despite global uncertainty. German CPI data released earlier showed that annual inflation in October eased from 2.4% to 2.3% (vs. 2.2% forecast), while the monthly rate rose from 0.2% to 0.3%. Meanwhile, eurozone GDP expanded 0.2% quarter-over-quarter but slowed year-over-year from 1.5% to 1.3% (1.2% expected). The U.S. dollar, on the other hand, strengthened on optimism surrounding the preliminary outcome of the Trump–Xi trade talks at the APEC summit. President Trump announced that tariffs on Chinese goods will be cut by 10%, and the additional 100% tariffs scheduled for November 1 were canceled. In return, Beijing agreed to allow U.S. soybean imports and postpone export restrictions on rare-earth metals.

GBP/USD

The pound continues to weaken against the U.S. dollar, testing 1.3150 to the downside and hovering near the April 14 low updated earlier this week. The pair is heading into the weekend under heavy pressure, as the dollar remains broadly supported despite the Federal Reserve’s recent rate cut. The greenback advanced further after the Trump–Xi talks, as Washington decided to pause additional tariff hikes planned for early November, while China delayed its rare-earth export tightening measures.

Meanwhile, expectations of a rate cut by the Bank of England at its November 6 meeting are increasing. The decision will largely depend on inflation dynamics, which remain moderate: CPI held steady at 3.8% y/y in September, while the monthly reading fell from 0.3% to 0.0% (vs. a forecast for 4.0% y/y). The pound received slight support from September retail sales, which rose 1.5% y/y (vs. 0.6% expected) and slipped only 0.5% m/m (vs. –0.2% expected). Business activity indicators also improved: the S&P Global Manufacturing PMI jumped from 46.2 to 49.6 (46.6 forecast), while the Services PMI edged up from 50.8 to 51.1 (51.0 expected).

AUD/USD

The Australian dollar shows a slight decline against the U.S. dollar, trading near 0.6550 as the week concludes almost flat. The movement follows mixed Chinese data: the NBS Manufacturing PMI fell from 49.8 to 49.0 (49.6 expected), while the Services/Construction PMI rose marginally from 50.0 to 50.1. Domestically, Australia’s Producer Price Index rose 3.5% y/y (from 3.4%) and 1.0% q/q (from 0.7%, vs. 0.8% forecast).

Earlier, Australian inflation data for Q3 reinforced expectations that the Reserve Bank of Australia (RBA) will avoid immediate easing. The core CPI accelerated y/y from 2.7% to 3.0% and q/q from 0.7% to 1.0%, above 0.8% expectations. The broader CPI rose y/y from 2.1% to 3.2% and q/q from 0.7% to 1.3%. Meanwhile, the U.S. dollar strengthened after the Fed cut its rate by 25 basis points and signaled that December easing is “not predetermined.” Nonetheless, analysts still expect another cut before year-end, with some forecasting a larger 50-basis-point move. The Fed continues to operate under limited data availability due to the government shutdown, which has suspended official labor reports.

USD/JPY

The U.S. dollar is showing slight weakness against the Japanese yen, retreating from February highs and testing the 154.00 level to the downside. Investors are focused on fresh Japanese macro data. Tokyo’s October CPI rose from 2.5% to 2.8% (y/y), beating the 2.6% forecast; core inflation excluding food and energy also climbed from 2.5% to 2.8%. The pickup in inflation may strengthen the Bank of Japan’s case for tightening monetary policy. However, markets remain cautious under Prime Minister Sanae Takaichi, known for her support of a dovish stance and fiscal stimulus.

Industrial production data for September also surprised positively: output rose 3.4% y/y (after –1.6%), and 2.2% m/m (after –1.5%, vs. 1.5% expected). Retail sales climbed 0.5% after –1.1% previously (0.7% forecast). The Bank of Japan kept its rate unchanged at 0.50% as expected, while the Fed earlier cut its benchmark by 25 bps to 4.00%, signaling possible further easing pending a comprehensive review of incoming data.

XAU/USD

Gold (XAU/USD) is consolidating near the 4,000.00 level after a sharp rally earlier in the week, driven mainly by technical factors amid a lack of fresh U.S. data due to the ongoing government shutdown. No progress has been made in negotiations between Democrats and Republicans, while President Trump remains on a diplomatic tour of Asia. The key event of the week was his meeting with Chinese President Xi Jinping, focused on resolving trade tensions.

Earlier, Trump had announced plans to impose an additional 100% tariff on Chinese imports starting November 1 in response to Beijing’s review of rare-earth export policy. Following the meeting, the U.S. agreed to suspend new tariffs for at least a year, while China postponed export restrictions. Although no joint statement was issued, Trump confirmed a 20% tariff reduction on Chinese goods. Gold also found support after the Fed’s rate cut of 25 basis points to 4.00%, accompanied by comments that inflation risks are contained and the labor market remains uncertain. Chair Jerome Powell cautioned markets against excessive expectations, emphasizing that December policy easing is “not predetermined.”