US markets are closed today for Martin Luther King Jr. Day, so investors are focusing on releases from Japan. November machinery orders fell 6.4% year-on-year after a 12.5% increase (versus a 4.9% forecast), and dropped 11.0% month-on-month after rising 7.0%, while industrial production eased from −2.1% to −2.2%.

Additional support for the yen still comes from expectations that the Bank of Japan could raise interest rates as early as April. However, tighter monetary policy conflicts with the agenda of Prime Minister Sanae Takaichi, who favors a more accommodative stance—a position that has been widely debated and criticized in recent months. This divergence has partly fueled talk of early parliamentary elections: Takaichi is considering dissolving the lower house and holding a vote as soon as February 2026 to strengthen her position and secure support for a broad economic program that would expand fiscal stimulus and reduce the tax burden. Markets reacted to these signals with a noticeable weakening of the yen: USD/JPY approached 160.00, and the currency has lost about 13.0% over the past eight months, reflecting expectations of continued dovish policy and higher budget spending. The macro backdrop adds pressure as well—by the end of 2025, inflation excluding fresh food was around 3.0% year-on-year, while real wages continued to decline, amplifying the negative effects of a weak currency and rising imported inflation. In this environment, investors fear that political uncertainty and potential delays in key budget decisions amid the election cycle could trigger new domestic stress and undermine the Bank of Japan’s efforts to support the economy and stabilize financial markets, keeping the risk of further yen weakness in place.

On Thursday at 01:50 (GMT+2), Japan will publish December foreign trade data: markets currently expect exports to increase by another 6.1%, while imports are forecast to ускориться from 1.3% to 3.6%. On Friday at 01:30 (GMT+2), investors will focus on December CPI figures, which could be one of the key signals for the Bank of Japan regarding further policy adjustments. On the same day, the central bank will hold its first interest-rate meeting of the year, and analysts are largely confident the rate will remain unchanged at 0.75%.

Global markets remain highly tense amid elevated import tariffs initiated by US President Donald Trump, who last week revived a hard line on Greenland and announced new 15.0% tariffs against Denmark and a number of other European countries that supported Copenhagen and sent military personnel to the island. The duties are expected to take effect on February 1, then rise to 25.0% in summer and remain in place until a final agreement on the US “acquisition” of Greenland is reached.

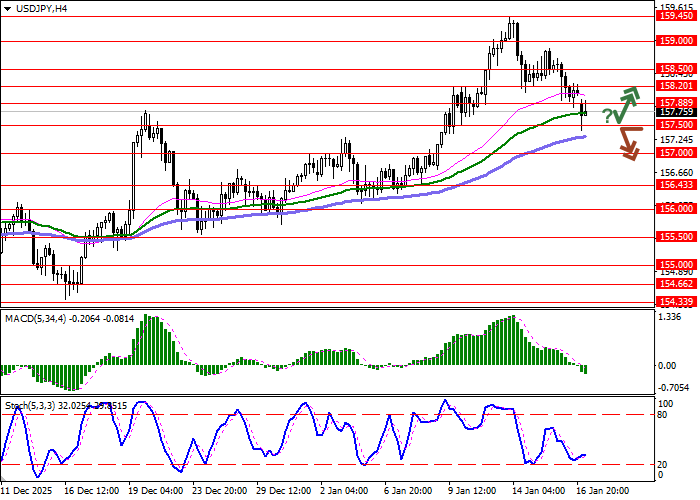

Support and resistance levels

On the daily chart, Bollinger Bands continue to rise steadily: the price range is расширяется, giving bulls room to push toward new local highs. MACD has turned lower, forming a fresh and robust sell signal (the histogram is trying to закрепиться below the signal line). Stochastic is declining more confidently and is now around the middle of its working range, pointing to sufficient potential for bearish momentum to develop.

Resistance levels: 157.88, 158.20, 158.50, 159.00.

Support levels: 157.50, 157.00, 156.43, 156.00.

Trading scenarios and USD/JPY forecast

Short positions can be opened after a confident downside break below 157.50, targeting 156.43. Stop loss: 157.88. Time horizon: 2–3 days.

A rebound from 157.50 as support followed by an upside break above 157.88 could signal new long positions, targeting 159.00. Stop loss: 157.50.

Scenario

| Timeframe | Intraday |

| Recommendation | SELL STOP |

| Entry point | 157.50 |

| Take Profit | 156.43 |

| Stop Loss | 157.88 |

| Key levels | 156.00, 156.43, 157.00, 157.50, 157.88, 158.20, 158.50, 159.00 |

Alternative scenario

| Recommendation | BUY STOP |

| Entry point | 157.90 |

| Take Profit | 159.00 |

| Stop Loss | 157.50 |

| Key levels | 156.00, 156.43, 157.00, 157.50, 157.88, 158.20, 158.50, 159.00 |