In particular, this view was reinforced by inflation data released the day before. In November, the headline Consumer Price Index slowed on a year-over-year basis from 3.0% to 2.7%, compared with forecasts of 3.1%, while core inflation excluding food and energy eased from 3.0% to 2.6%. Investors also focused on jobless claims data: for the week ending December 12, initial claims declined from 237.0K to 224.0K versus expectations of 225.0K, while continuing claims rose from 1.830M to 1.897M, below the projected increase to 1.940M.

Later today at 17:00 (GMT+2), updated inflation expectations from the University of Michigan will be released. These are expected to remain unchanged at 4.1% for one-year expectations and 3.2% for five-year expectations. The consumer expectations index for December is forecast at 55.0 points, while the consumer sentiment index may edge slightly higher from 53.3 to 53.4 points.

Earlier, in an interview with CNBC, Christopher Waller, a candidate for the position of Fed Chair, stated that maintaining a dovish policy stance remains appropriate. At the same time, he noted that current policy settings remain up to 100 basis points above the neutral level, at which the central bank neither restrains economic growth nor adds inflationary pressure—an assessment he described as supportive for the economy under current conditions.

Market attention today will also focus on Canadian retail sales data for October, due at 15:30 (GMT+2). On a monthly basis, headline retail sales are expected to show flat growth after a decline of 0.7% previously, while sales excluding autos may rise by 0.2%. In addition, data on new housing price indices will be released, with forecasts pointing to a recovery to 0.0% in November after a 0.4% decline in the prior month.

Earlier this week, Canadian inflation figures were published. The Bank of Canada’s core CPI increased by 2.9% year-over-year in November, while slowing on a monthly basis from 0.6% to –0.1%. The broader CPI measure held steady at 2.2% annually and eased slightly from 0.2% to 0.1% month-over-month.

Market participants also noted the Bank of Canada’s assessment highlighting continued uncertainty around the economy’s response to elevated trade tariffs. The central bank pointed to volatility in quarterly GDP and trade, as well as ongoing weakness in the labor market, although the unemployment rate declined to 6.5% in November after peaking at 7.1% in September. Inflation stood at 2.2% in October, while core inflation remains near 2.5%. Officials acknowledge that tax measures introduced last year may cause short-term fluctuations, but believe that economic slowdown will offset rising costs and keep inflation close to the 2.0% target.

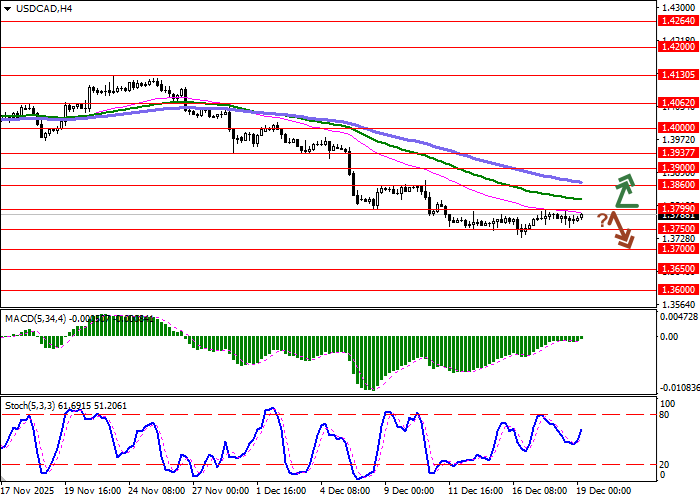

Support and Resistance Levels

On the daily chart, Bollinger Bands are showing a confident downward slope, with the price range narrowing and reflecting mixed short-term trading conditions. The MACD has turned higher, generating a fresh buy signal as the histogram moves above the signal line. The Stochastic oscillator is showing stronger upward momentum and is rapidly approaching overbought territory, indicating increased risks of short-term overbought conditions for the US dollar.

Resistance levels: 1.3799, 1.3860, 1.3900, 1.3937.

Support levels: 1.3750, 1.3700, 1.3650, 1.3600.

Trading Scenarios and USD/CAD Forecast

Long positions can be considered after a confident breakout above the 1.3799 resistance level, with a target at 1.3900. Stop-loss — 1.3750. Time horizon: 1–2 days.

A rejection from the 1.3799 resistance level followed by a downside breakout below 1.3750 may signal new short positions targeting 1.3650. Stop-loss — 1.3799.