Today at 15:00 (GMT+2), market participants will focus on the March house price index, which reflects the average price change in repeat home sales or revaluations of the same property. The monthly indicator is expected to rise by 0.1% after remaining unchanged earlier, while the annual S&P/Case-Shiller index may increase from 0.9% to 1.0%. In addition, traders will assess consumer confidence data, where the indicator is forecast to slow from 92.8 points to 91.9 points. However, the most important statistics capable of affecting the pair’s dynamics will arrive only at the end of the week, when Germany releases April labor market data. Current forecasts suggest that the number of unemployed people may decline from 20.0K to 11.0K, while the unemployment rate is expected to remain unchanged at 6.4%.

One of the main sources of market uncertainty remains the Middle East crisis, where recent developments have suggested possible progress toward de-escalation. According to reports from The Washington Post and The New York Times, the United States and Iran have developed a memorandum of understanding that would extend the ceasefire for 60 days and provide for the gradual reopening of the Strait of Hormuz, a key maritime route through which around 20.0% of global energy supplies were transported before the conflict. Diplomatic sources indicate that, after the peace plan is signed, Iran’s Islamic Revolutionary Guard Corps would immediately unblock the waterway and take steps to restore shipping to pre-war levels within 30 days. At the same time, both sides would announce the suspension of military operations on all fronts, including Lebanon.

However, optimism remains cautious. Progress has so far been mainly reported by White House representatives, while Iranian officials have taken a more restrained position. Iran’s Foreign Ministry spokesperson Esmail Baghaei said that Tehran excludes the issue of control over the Strait of Hormuz from the memorandum, stressing that this matter should be decided only by the coastal states of the region. He also noted that it is still too early to speak about the imminent signing of an agreement, as the current consultations do not yet include the nuclear issue, which the sides plan to discuss only within 60 days after the framework document is approved. Meanwhile, U.S. Secretary of State Marco Rubio, during his visit to New Delhi, stated that Washington would either reach a “beneficial deal” or act in another way, while emphasizing that diplomacy remains the priority for the Republican administration.

Meanwhile, pressure on the single currency is still coming from weak macroeconomic data. Preliminary business activity indices published last week showed a sharp decline in economic activity in May. The composite PMI fell to 47.5 points, the lowest level since October 2023, against expectations of 48.8 points. The services PMI dropped to 46.4 points, the lowest level since February 2021 excluding the COVID-19 pandemic period, indicating a rapid decline in consumer demand caused by the rising cost of living. The manufacturing PMI also weakened to 51.4 points from 52.2 points a month earlier, missing expectations. Against this background, the eurozone economy may contract by 0.2% in the second quarter, and recession risks could increase further if negotiations with Iran last longer than expected or energy prices remain elevated.

At the same time, the International Monetary Fund, in analytical materials presented to eurozone finance ministers at an informal meeting in Nicosia, warned of growing fiscal risks in the region. The IMF noted that, if current budget policies continue without structural adjustments, public debt could move onto a steadily rising and potentially unstable trajectory. The debt of an average European economy could reach around 130.0% of GDP by 2040, roughly twice the current level. In an environment of elevated interest rates, rising defense spending, and large-scale green energy costs, fiscal space is narrowing rapidly. This increases the need for budget consolidation, optimization of public spending, and structural reforms aimed at accelerating economic growth. Discussions also highlighted the limited effectiveness of traditional fiscal adjustment tools and the growing importance of coordination at the EU level, including possible joint borrowing mechanisms and redistribution of investment burdens.

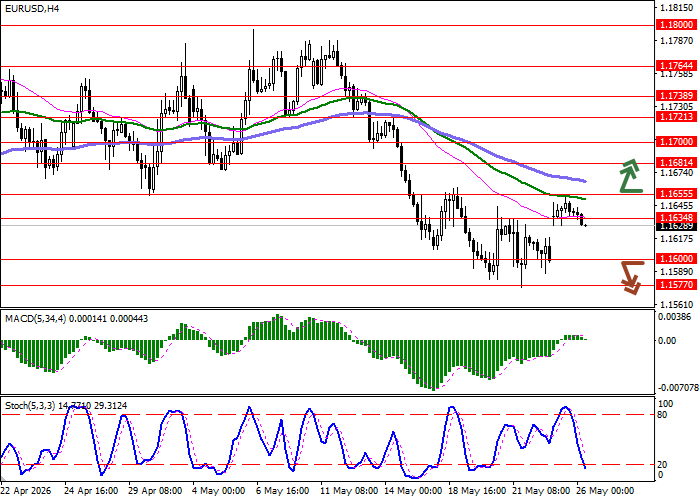

Support and resistance levels

On the daily chart, Bollinger Bands show a moderate decline: the price range is narrowing but remains wide enough for the current level of market activity. MACD is turning upward, forming a new buy signal and attempting to move above the signal line. The Stochastic indicator is rapidly approaching its upper values, pointing to short-term overbought risks for the euro.

Resistance levels: 1.1634, 1.1655, 1.1681, 1.1700.

Support levels: 1.1600, 1.1577, 1.1529, 1.1500.

EUR/USD trading scenarios and forecast

Short positions may be considered after a confident breakout below 1.1600, with a target at 1.1529. Stop-loss — 1.1634. Expected timeframe: 2–3 days. A return of bullish momentum followed by a breakout above 1.1655 may become a signal for long positions with a target at 1.1700. Stop-loss — 1.1634.

Scenario

| Timeframe | Intraday |

| Recommendation | SELL STOP |

| Entry point | 1.1595 |

| Take Profit | 1.1529 |

| Stop Loss | 1.1634 |

| Key levels | 1.1500, 1.1529, 1.1577, 1.1600, 1.1634, 1.1655, 1.1681, 1.1700 |

Alternative scenario

| Recommendation | BUY STOP |

| Entry point | 1.1660 |

| Take Profit | 1.1700 |

| Stop Loss | 1.1634 |

| Key levels | 1.1500, 1.1529, 1.1577, 1.1600, 1.1634, 1.1655, 1.1681, 1.1700 |