Last week, the yen received moderate support from Jibun Bank business activity data, which confirmed that the Japanese economy is actively emerging from a prolonged period of stagnation. The manufacturing index accelerated to 53.0 points, while the services index rose to 53.8 points, signaling expanding domestic demand. At the same time, the composite indicator held at 53.9 points, its highest level in nearly two years, pointing to the economy’s ability to adapt to tighter monetary conditions.

At the same time, more mixed data from the middle of last week — falling leading indicators alongside rising coincident indicators — reflected the transitional nature of the current cycle. The economy is already showing strength in the present, but doubts remain about the sustainability of the momentum. Bank of Japan rhetoric following the March 19 meeting continues to have a significant effect on the market. Despite keeping the interest rate at 0.75%, investors interpret the current pause as temporary. Expectations for policy changes at upcoming meetings remain significant, though not fully confirmed by actual signals. The Bank of Japan is likely to act slowly and predictably, reducing the probability of a sharp yen rally without additional triggers.

For now, Japanese authorities have turned to the International Energy Agency (IEA) with a request for an additional coordinated release of strategic reserves. During talks with IEA Executive Director Fatih Birol, Economy and Industry Minister Ryosei Akazawa stressed that shortages of fuel and raw materials in Asia could seriously disrupt global manufacturing supply chains, especially in countries dependent on exports from the region. It should be recalled that in early March, IEA member countries agreed to the largest release in the agency’s history — 400.0 million barrels, or around 20.0% of combined strategic reserves — while leaving 80.0% untouched. This decision came in response to the escalation of the US-Iran conflict, which put pressure on global oil prices and raised import costs for fuel-dependent countries such as Japan, where 95.0% of consumption comes from the Middle East. In response to the “energy shock,” the government began releasing private-sector reserves equivalent to 15 days of supply, to be followed by state reserves. Together with IEA measures, this is aimed at stabilizing the domestic market and preventing unprecedented pressure on industry and logistics, including rising fuel prices and lower profitability across production chains. As a result, the preservation of most reserves (80.0%) and the readiness for further IEA action provide a limited but critically important buffer against sharp oil price swings and potential yen depreciation.

Investor attention this week is focused on March US labor market data, which could become a key driver for reassessing expectations around Federal Reserve policy. The previous report showed a notable deterioration in employment dynamics: in February, the economy lost 92.0 thousand jobs, marking the first significant sign of labor market cooling in recent months. The consensus forecast for March suggests a moderate recovery, but the range of estimates remains wide — from 20.0 thousand to 60.0–70.0 thousand — reflecting high uncertainty. The unemployment rate is expected to remain in the 4.4–4.5% range, signaling a labor market entering a “low hiring, low firing” phase. This configuration is not a direct recession signal, but it does indicate a loss of positive momentum and a weaker contribution from employment to economic growth, which could strengthen expectations of easier monetary policy and put short-term pressure on the US dollar.

An additional factor for global markets will be Japan’s macroeconomic data due on March 31, including inflation and industrial production. Core consumer inflation (excluding fresh food and energy) is expected to come in around 1.8% year-on-year, remaining below the Bank of Japan’s target. At the same time, industrial activity is expected to deteriorate sharply: according to preliminary estimates, production volumes may decline by 2.1% month-on-month after rising 4.3% previously. Taken together with moderate inflation, this limits the room for the Bank of Japan to tighten policy and has a restrained impact on the yen.

Support and resistance levels

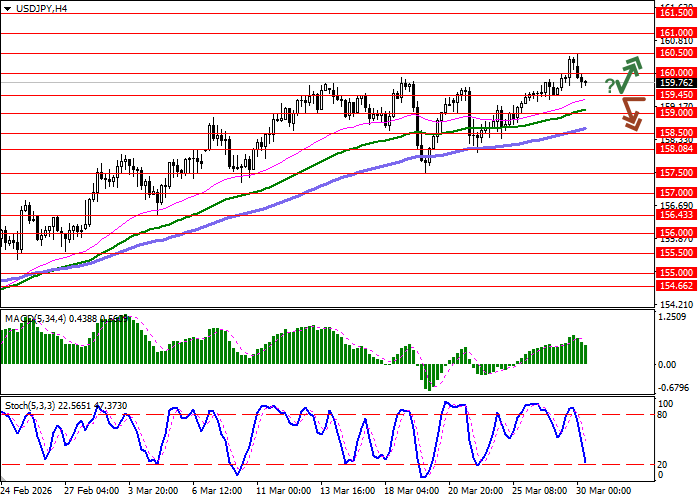

On the daily chart, Bollinger Bands are turning into a horizontal plane, leaving enough room for a modest short-term correction lower. MACD is rising, maintaining a weak buy signal and staying above the signal line. Stochastic, after reaching peak values, is turning downward, indicating risks of overbought conditions for the US dollar in the very short term.

Resistance levels: 160.00, 160.50, 161.00, 161.50.

Support levels: 159.45, 159.00, 158.50, 158.08.

Trading scenarios and USD/JPY forecast

Short positions may be opened after a confident break below 159.45 with a target at 158.50. Stop-loss — 160.00. Timeframe: 1–2 days. A rebound from 159.45 as support, followed by a breakout above 160.00, may become a signal to open new long positions with a target at 161.00. Stop-loss — 159.45.

Scenario

| Timeframe | Intraday |

| Recommendation | SELL STOP |

| Entry point | 159.40 |

| Take Profit | 158.50 |

| Stop Loss | 160.00 |

| Key levels | 158.08, 158.50, 159.00, 159.45, 160.00, 160.50, 161.00, 161.50 |

Alternative scenario

| Recommendation | BUY STOP |

| Entry point | 160.05 |

| Take Profit | 161.00 |

| Stop Loss | 159.45 |

| Key levels | 158.08, 158.50, 159.00, 159.45, 160.00, 160.50, 161.00, 161.50 |