Due to growing geopolitical tensions and risks of disruptions to oil supplies through key routes, including the Strait of Hormuz and the Bab-el-Mandeb Strait, France is taking preventive measures to stabilize its domestic energy market. Particular importance is attached to the Gravenchon refinery, which accounts for around 20.0% of national refining capacity and up to 12.0 million tons of petroleum products annually. Its utilization helps partially offset supply shortages, especially amid higher freight and insurance costs caused by extended logistics routes. In addition, this step is necessary to protect jobs and ensure stable functioning of the national economy.

This week, a set of preliminary macroeconomic data was released, pointing to persistent risks. France’s manufacturing PMI stood at 50.2 points in March, slightly above the previous 50.1, while the services PMI fell to 48.3 from 49.6. Against this backdrop, the composite indicator from S&P Global declined from 49.9 to 48.3. The negative trend is becoming systemic, confirmed by deterioration in leading indicators: new orders fell at the fastest pace since July 2025, signaling further weakening of domestic and corporate demand, while export orders declined at the fastest pace in 15 months, reflecting pressure from global conditions and energy costs. According to data from the National Institute of Statistics and Economic Studies (INSEE), the business climate index dropped to 99.0 from 102.0, while consumer confidence declined from 91.0 to 89.0.

It is also worth noting that short-term bond auctions were held earlier this week: 3- and 6-month securities were placed at yields of 2.226% and 2.412%, significantly higher than the previous 2.108% and 2.199%, while 12-month bonds were placed at 2.585% compared to 2.353% earlier. As for long-term bonds, after reaching an interim high of 2.670%, yields consolidated briefly, and today one-year bonds are again trading near 2.717%, well above last Friday’s 2.586%. Ten-year bonds rose to 3.796% from 3.643%, while 20- and 30-year yields reached 4.293% and 4.550% compared to 4.155% and 4.437%, respectively.

Top gainers in the index include TotalEnergies SE (+2.89%), STMicroelectronics NV (+1.91%), Sanofi SA (+1.36%), Dassault Systèmes SE (+0.95%), and Carrefour Group SA (+0.91%).

Among the biggest decliners are Pernod Ricard SA (–5.73%), Legrand SA (–4.50%), Schneider Electric SE (–3.93%), ArcelorMittal SA (–3.47%), and Airbus Group SE (–3.00%).

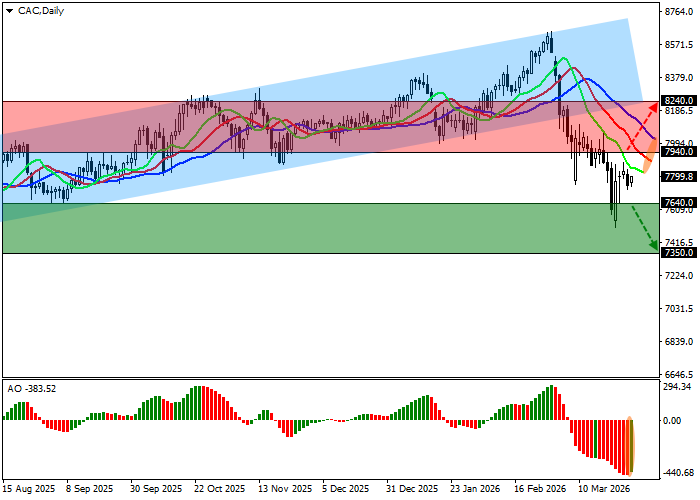

Support and resistance levels

On the daily chart, the instrument continues its local correction, still trading well below the support line of the ascending channel with dynamic boundaries at 8700.0–8050.0.

Technical indicators maintain a local sell signal received at the beginning of the month: fast EMAs on the Alligator indicator are widening the fluctuation range, while the AO histogram forms corrective bars below the transition level.

Support levels: 7640.0, 7350.0.

Resistance levels: 7940.0, 8240.0.

Trading scenarios and CAC 40 outlook

Short positions may be opened after consolidation below 7640.0 with a target at 7350.0. Stop-loss — 7800.0. Implementation period: 7 days or more.

Long positions may be opened after consolidation above 7940.0 with a target at 8240.0 and stop-loss at 7850.0.

Scenario

| Timeframe | Weekly |

| Recommendation | SELL STOP |

| Entry Point | 7639.5 |

| Take Profit | 7350.0 |

| Stop Loss | 7800.0 |

| Key Levels | 7350.0, 7640.0, 7940.0, 8240.0 |

Alternative Scenario

| Recommendation | BUY STOP |

| Entry Point | 7940.5 |

| Take Profit | 8240.0 |

| Stop Loss | 7850.0 |

| Key Levels | 7350.0, 7640.0, 7940.0, 8240.0 |