According to Axios, despite the White House previously announcing a ceasefire to allow bilateral consultations with Iranian representatives aimed at defining the key terms of a future peace plan, some US officials believe President Donald Trump could order a resumption of hostilities this week if no progress is made in the negotiations.

Following reports of Islamic Revolutionary Guard Corps (IRGC) drone and ballistic missile strikes on the United Arab Emirates (UAE) last Monday, authorities declared a serious escalation of the conflict and reserved the right to take retaliatory measures.

At the same time, Donald Trump stated in an interview on The Hugh Hewitt Show that resolving the Middle East crisis would take two to three weeks, while emphasizing that the armed forces have no strict time limits for completing all assigned objectives during the special operation. According to the unofficial analytical project Iran War Cost Tracker, total White House expenditure on the operation has already exceeded $70.8 billion — a figure that will undoubtedly weigh on the Republican Party's approval ratings.

The key driver of stock market growth at present is the Q1 earnings season that began in late April. Financial conglomerate HSBC Holdings Plc reported revenue of €16.33 billion — well below €24.41 billion a year ago but above the €15.00 billion posted in the previous period — while earnings per share (EPS) reached €0.342, compared to €0.390 and €0.302 respectively. Bayerische Motoren Werke AG (BMW) management reported revenue of €32.29 billion, below €33.76 billion and €33.45 billion in prior periods, with EPS of €2.40 versus €3.38 and €2.92 respectively.

The current situation in the bond market is not conducive to a recovery in demand for risk assets, as yields across the full range of leading bonds are in the green this week: one-year paper is trading at 2.526%, slightly above last week's closing level of 2.498%, 10-year bonds are at 3.066% versus 3.033%, and 20-year and 30-year bonds are at 3.515% and 3.584% compared to 3.474% and 3.545% respectively.

Top gainers in the index include Infineon Technologies AG (+6.50%), Commerzbank AG (+4.50%), Siemens AG (+4.39%), Rheinmetall AG (+3.40%), and Siemens Energy AG (+3.26%).

Leading decliners include Fresenius Medical Care AG & Co. KGaA (–10.68%), Fresenius SE & Co. KGaA (–3.36%), Deutsche Börse AG (–1.53%), Deutsche Post AG (–0.96%), and Zalando SE (–0.57%).

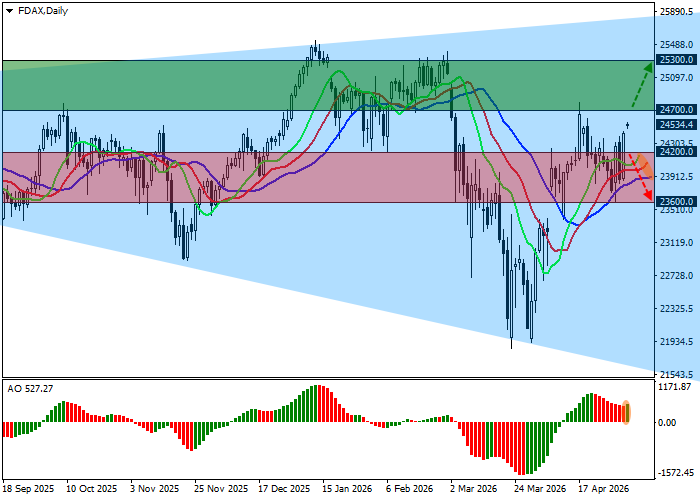

Support and Resistance Levels

On the daily chart, the price is trading in a corrective trend, once again pulling back from the support line of an "expanding formation" pattern with boundaries at 26000.0–21800.0, which began forming in mid-2025.

Technical indicators are maintaining the buy signal generated in early April: the fast EMAs on the Alligator indicator are holding above the signal line, while the AO histogram is forming corrective bars in the buy zone.

Support levels: 24200.0, 23600.0.

Resistance levels: 24700.0, 25300.0.