In its latest report, CryptoQuant Head of Research Julio Moreno said that Strategy’s STRC preferred shares had broken below USD 83, falling to USD 82.50 — a 17.5% discount to their USD 100 par value and the deepest discount since the product was issued. The continued decline in STRC has prompted increasing comparisons with the type of downward spiral that contributed to the collapse of the Terra-Luna ecosystem in 2022.

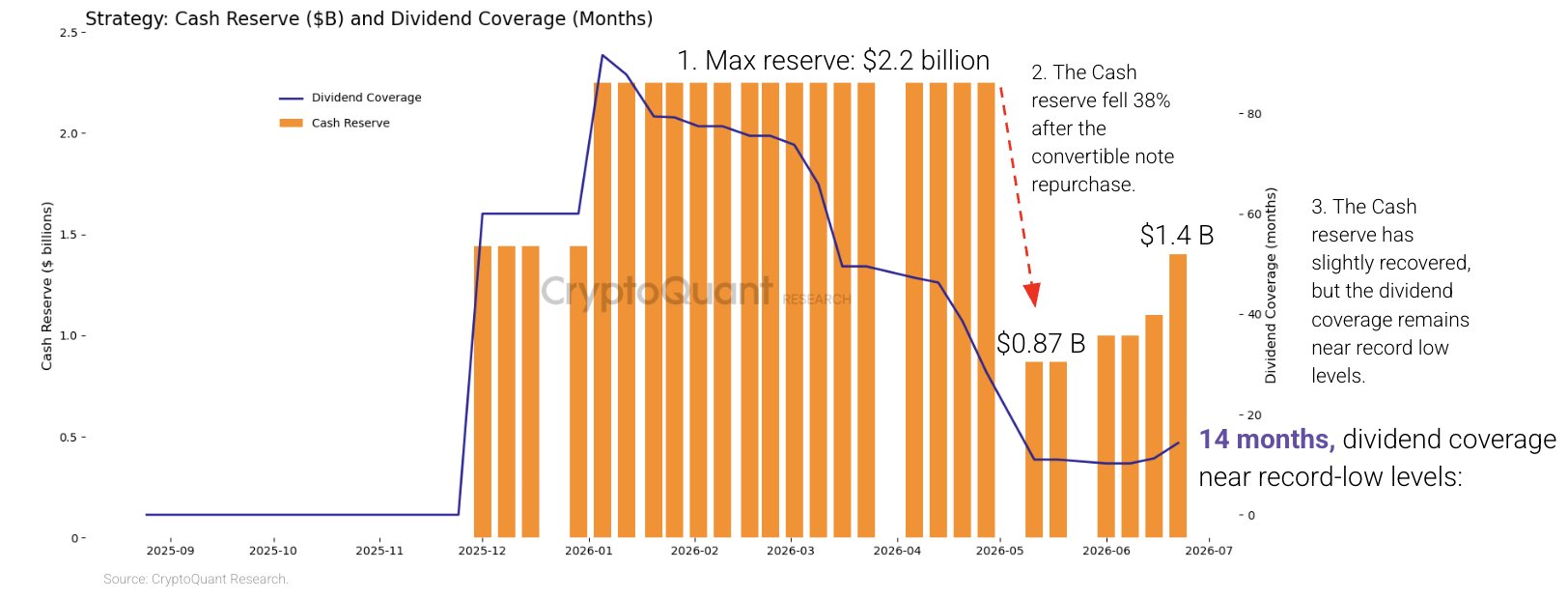

According to Moreno, Strategy’s main problem is not Bitcoin itself but liquidity. Since the beginning of 2026, the company’s cash balance has fallen by 38%, partly because Strategy spent USD 1.5 billion to redeem convertible notes due in 2029 ahead of schedule. As the cash buffer continues to shrink, dividend obligations are growing at an alarming pace.

To continue raising capital for Bitcoin purchases, Strategy has repeatedly issued STRC, increasing total annual dividend obligations from USD 300 million at the start of the year to USD 1.2 billion currently. In less than six months, the payment burden has nearly quadrupled.

At the beginning of the year, the company’s cash reserves were enough to cover dividends for more than seven years. Now, that period has fallen to only 14 months. CryptoQuant estimates that Strategy would need to raise cash reserves to USD 2.8 billion to restore its dividend coverage period to 24 months, almost twice the amount of cash currently available.

Concerns intensified after Strategy sold Bitcoin for the first time since 2022, a move that JPMorgan reportedly described as potentially unsettling for the market. The transaction involved only 32 BTC and had little financial significance, but the company’s first break from its “never sell” principle raised doubts about whether liquidity pressure may be greater than management has acknowledged.

Scepticism has also spread among Strategy shareholders. Some investors have criticised management for underestimating the potential risks of STRC. Others argue that the current model is becoming increasingly dependent on issuing new securities to maintain the fundraising cycle that supports Strategy’s Bitcoin acquisition strategy.

Strategy’s Real Vulnerability

Strategy owns the largest Bitcoin treasury among publicly listed companies, but Bitcoin itself does not generate cash flow to pay dividends, service debt, or strengthen liquidity.

The value of its holdings may rise substantially over time, but financial obligations arise every quarter. This is Strategy’s real vulnerability.

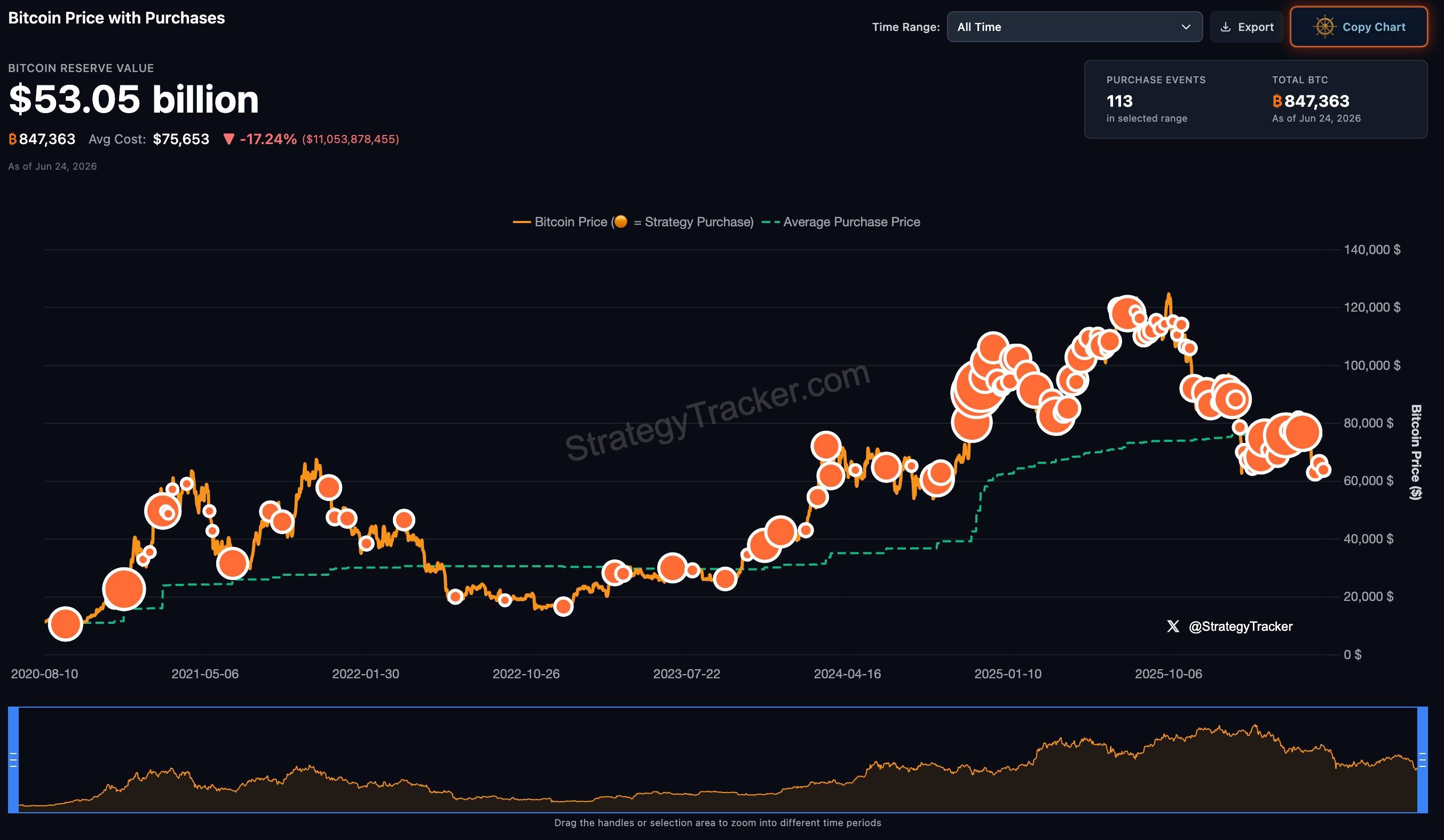

CryptoQuant believes that selling Bitcoin to replenish cash reserves at this stage would be extremely risky. The entire BTC position, worth around USD 53 billion and accumulated during 2024–2026, is reportedly below its cost basis, creating unrealised losses of nearly USD 11 billion.

This means that any large-scale Bitcoin sale at current price levels could turn paper losses into realised losses, directly reducing shareholder value and weakening the investment narrative Michael Saylor has built over many years.

CryptoQuant’s second recommendation is for Strategy to develop a more systematic Bitcoin purchasing model. Moreno argues that Strategy’s habit of buying regardless of market conditions has become a common “meme” in the crypto community, as many purchases have been made near short-term price peaks.

In his view, buying whenever capital is available is not a sustainable investment strategy and may lead to accumulating assets at unfavourable price levels.

The third recommendation runs directly against Michael Saylor’s long-standing philosophy: establish a mechanism for taking partial profits during future Bitcoin bull cycles in order to realise gains, reduce leverage, and build cash reserves for market downturns.

This context is causing investors to focus increasingly on Strategy’s capital structure rather than the amount of Bitcoin it holds. The company has issued around USD 15 billion in preferred shares, with STRC alone accounting for roughly USD 9 billion.

Annual dividend obligations across all preferred share classes have risen to around USD 1.7 billion, while the company’s core software business does not generate enough profit to cover these costs independently.

Although Michael Saylor continues to express confidence in the long-term Bitcoin strategy, the main question is whether Strategy has enough time and liquidity to wait for the next Bitcoin growth cycle.

If Bitcoin enters a new bullish phase soon, Saylor’s model may once again be validated. However, if the market remains sideways or weak for several more quarters, dividend obligations and cash constraints could become a severe burden for the company’s Bitcoin empire.