Nevertheless, last week ECB Executive Board member Isabel Schnabel stated that no changes in interest rates are expected in the foreseeable future and that the current level of 2.15% is likely to be maintained in the absence of force-majeure events that could affect the economy. Earlier comments from the official had been interpreted by investors as a signal of possible policy tightening next year. Schnabel stressed that her previous remarks referred not to the need for a hawkish stance, but rather to the lack of grounds for further rate cuts.

This shift in rhetoric was likely supported by a revision of the eurozone’s 2025 GDP growth forecast to 1.4%, up from the September estimate of 1.2%. The adjustment reflects a combination of factors pointing to more resilient economic conditions in the region than previously expected. In addition, according to data from the international consultancy Employment Conditions Abroad (ECA), which specializes in global mobility and expatriate management, real wages were indexed in nearly all EU countries covered by the study in 2025. Median real wage growth is projected at 1.4% in 2025 and 1.7% in 2026 across 25 EU member states. The main drivers behind the revision were improved macroeconomic indicators, signaling a gradual stabilization of business activity and a decline in trade policy uncertainty, which has enhanced investment and export expectations among companies. Experts expect Hungary, Poland, the Czech Republic, and Bulgaria to be among the leaders in terms of wage growth.

At the same time, the U.S. Federal Reserve assesses the domestic economy as expanding at a moderate pace and expects inflation to peak in the first three months, followed by a slowdown. The recent reduction in borrowing costs was driven by a weakening labor market: in November, non-farm payroll growth amounted to just 64.0 thousand, October recorded negative dynamics, and the data release itself was delayed due to a record-length government shutdown. Meanwhile, the Federal Open Market Committee’s (FOMC) December forecast assumes that borrowing costs will reach 3.25–3.50% by the end of 2026. This appears to be a fairly conservative scenario compared with derivatives market expectations, which price in one to two rate cuts of 25 basis points each. The FOMC’s long-term neutral rate is estimated at 3.00%, a factor that continues to support the U.S. equity market, although the closer rates move toward neutral, the less room this support has to expand.

Today at 11:00 (GMT+2) and 16:46 (GMT+2), market participants will focus on December manufacturing activity data for the eurozone and the United States. If the indicators rise from 49.2 points and 51.8 points respectively, this would support the positions of the respective national currencies.

Support and resistance levels

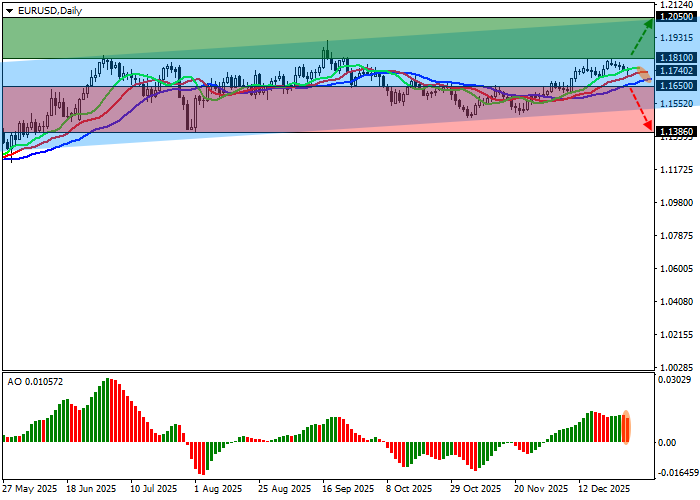

On the daily chart, the instrument remains in a corrective phase, once again approaching the resistance line of the ascending channel with dynamic boundaries at 1.2050–1.1540.

Technical indicators continue to signal a buy: the fast EMAs on the Alligator indicator are moving away from the signal line, widening the fluctuation range, while the AO oscillator histogram is forming new rising bars, increasing within the buying zone.

Support levels: 1.1650, 1.1386.

Resistance levels: 1.1810, 1.2050.

Trading scenarios and EUR/USD outlook

Long positions can be opened after a firm breakout above 1.1810, with a target at 1.2050. Stop-loss: 1.1740. Time horizon: 7 days or more.

Short positions can be opened after a firm move below 1.1650, with a target at 1.1386. Stop-loss: 1.1730.

Scenario

| Timeframe | Weekly |

| Recommendation | BUY STOP |

| Entry point | 1.1810 |

| Take Profit | 1.2050 |

| Stop Loss | 1.1740 |

| Key levels | 1.1386, 1.1650, 1.1810, 1.2050 |

Alternative scenario

| Recommendation | SELL STOP |

| Entry point | 1.1650 |

| Take Profit | 1.1386 |

| Stop Loss | 1.1730 |

| Key levels | 1.1386, 1.1650, 1.1810, 1.2050 |