Today at 15:15 (GMT+2), the market will receive four-week employment data from Automatic Data Processing (ADP), which will precede the September labour report from the US Department of Labor on Thursday at 15:30 (GMT+2). Forecasts suggest an increase of 50.0 thousand new jobs in the nonfarm sector after a rise of 22.0 thousand in the previous month, while average hourly earnings are expected to remain unchanged at 0.3% month-on-month and 3.7% year-on-year, and the unemployment rate at 4.3%.

In addition, statistics on jobless claims will be released: for the week ending 14 November, the number of initial claims may rise from 218.0 thousand to 227.0 thousand, while continuing claims could adjust from 1.926 million. At 10:30 (GMT+2), European Central Bank (ECB) President Christine Lagarde will speak and may clarify the outlook for further cuts in borrowing costs; however, the regulator is already close to completing the current cycle of monetary easing and has achieved a steady reduction in inflation risks in the region.

GBP/USD

The pound is trading with near-zero momentum in the GBP/USD pair, holding close to 1.3160: market activity remains subdued, as participants are reluctant to open new positions ahead of US macroeconomic data. On Thursday at 15:30 (GMT+2), the September labour market report will be released: forecasts suggest that the US economy will create 50.0 thousand new nonfarm payrolls, twice the 22.0 thousand recorded in August, while average hourly earnings are expected to remain unchanged at 0.3% month-on-month and 3.7% year-on-year, and the unemployment rate at 4.3%, which will influence the Federal Reserve’s rhetoric.

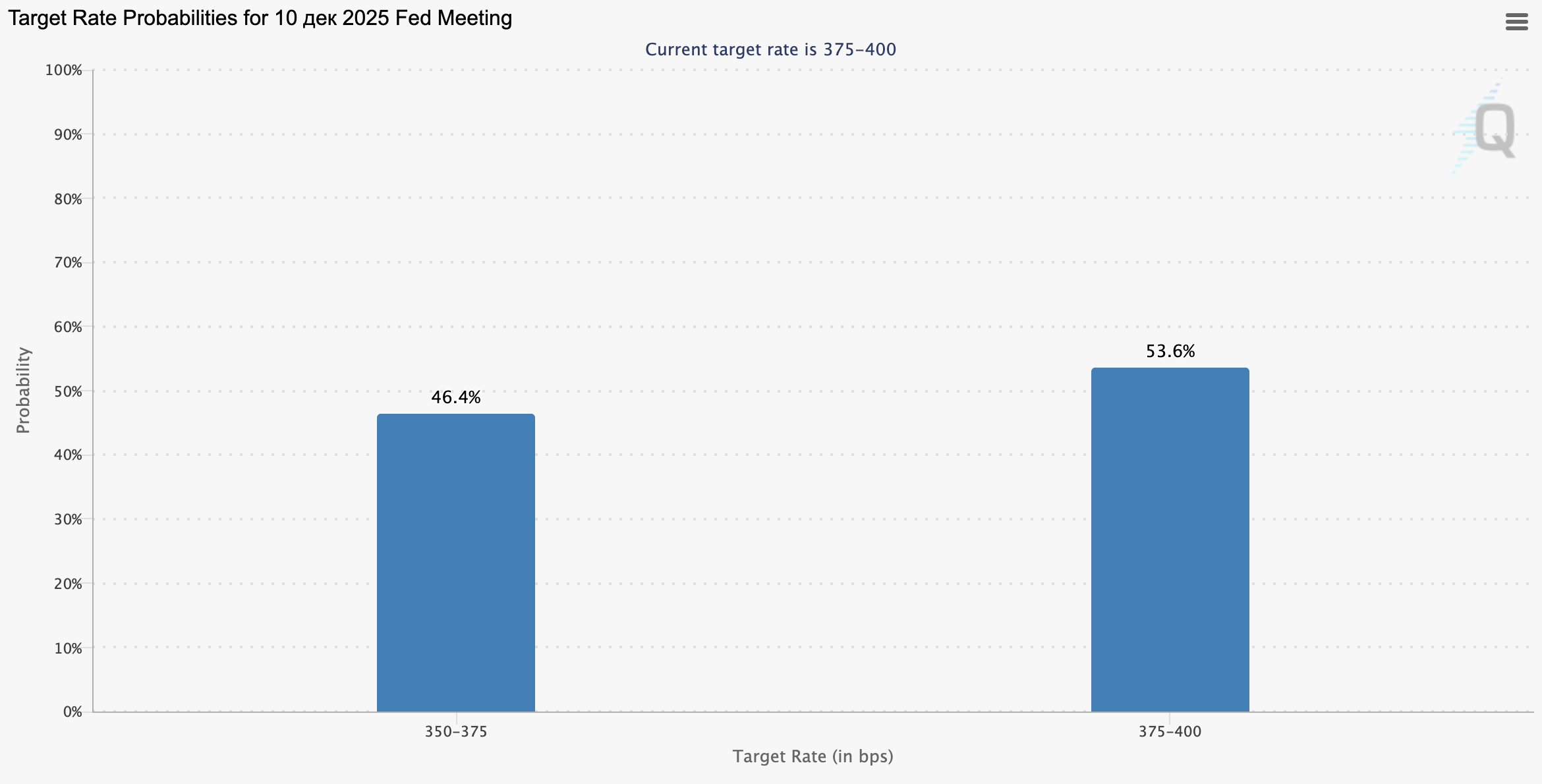

As a reminder, according to the Chicago Mercantile Exchange (CME Group) FedWatch Tool, the probability that monetary authorities will decide to cut the interest rate by 25 basis points at the December meeting has fallen from 66.9% to 48.6%. In the UK, on Wednesday at 09:00 (GMT+2), investors will evaluate October inflation data, which could strengthen expectations of possible monetary easing by the Bank of England: the annual consumer price index is likely to slow from 3.8% to 3.6%, while the monthly figure is expected to rise from 0.0% to 0.4%, and core inflation to ease from 3.5% to 3.4%. In addition, retail price index data will be released: in annual terms it may decline from 4.5% to 4.3%, while the monthly reading is expected to remain in negative territory.

NZD/USD

The New Zealand dollar is losing value against the US currency in the NZD/USD pair, testing the 0.5650 level: the US dollar is supported by revised expectations regarding additional monetary easing by the Federal Reserve, while the issue of a December rate cut remains unresolved, as policymakers’ rhetoric will depend on incoming macroeconomic data following the record-long government shutdown. The Senate and the House of Representatives managed to approve an updated bill on temporary funding of the federal government through the end of January 2026, but many analysts do not rule out new pauses in its work, given ongoing disagreements between Democrats and Republicans on key issues.

Meanwhile, the pair received some support earlier in the week from New Zealand data: the Business NZ services PMI rose from 48.3 points to 48.7 points in October. On Thursday at 23:45 (GMT+2), October trade data will be released: the previous report showed a moderate narrowing of the trade deficit from –4.12 billion dollars to –2.25 billion dollars. In the US, on Thursday at 15:30 (GMT+2), September labour market figures will be published: forecasts suggest that the national economy will create 50.0 thousand new nonfarm jobs, twice the 22.0 thousand recorded in August, with average hourly earnings unchanged at 0.3% month-on-month and 3.7% year-on-year, and the unemployment rate at 4.3%.

USD/JPY

The US dollar is showing sideways dynamics in the USD/JPY pair, holding near 155.00 and close to the record February highs. The yen remains under pressure amid growing concerns over new fiscal measures from the administration of Prime Minister Sanae Takaichi, who is known as a supporter of loose monetary policy and has previously signalled plans for broad tax incentives to stimulate domestic consumption and investment. Forex traders expect her to unveil her first economic stimulus package later this week.

Macroeconomic data released yesterday showed that industrial production accelerated in September, rising from 3.4% to 3.8% year-on-year and from 2.2% to 2.6% month-on-month, while third-quarter GDP contracted by 0.4% after a 0.6% increase previously, compared with a forecast of –0.6%. In the US, a batch of September labour market data that was delayed by the shutdown is due on Thursday at 15:30 (GMT+2). According to forecasts, the number of new nonfarm jobs will rise by 50.0 thousand after a gain of 22.0 thousand in the prior month, average hourly earnings will remain at 0.3% month-on-month and 3.7% year-on-year, signalling further stabilisation of inflationary pressures, and the unemployment rate at 4.3%. In addition, weekly jobless claims statistics will be released: for the week ending 14 November, initial applications are expected to increase from 218.0 thousand to 227.0 thousand, while continuing claims could adjust from 1.926 million.

XAU/USD

The XAU/USD pair is declining in value, extending last week’s corrective movement: the instrument is testing the 4020.00 level for a downside breakout as investors actively lock in long profits and reassess the outlook for further interest-rate cuts by the Federal Reserve. Now that the federal government has resumed work after the record shutdown, market attention is shifting back to macroeconomic indicators, particularly labour market data.

On Thursday at 15:30 (GMT+2), the September jobs report will be released, which will remain an important input for the Fed’s decision-making: forecasts suggest that the US economy will create 50.0 thousand new nonfarm jobs, twice the 22.0 thousand recorded in August, with average hourly earnings unchanged at 0.3% month-on-month and 3.7% year-on-year, and the unemployment rate at 4.3%. As a reminder, according to the Chicago Mercantile Exchange (CME Group) FedWatch Tool, the probability of a 25-basis-point rate cut at the December meeting has dropped from 66.9% to 48.6%. Earlier, Fed Chair Jerome Powell stressed that easing is not predetermined and even described it as risky in light of signs of strengthening inflation.