In focus for investors and forex traders are the prospects of ending the government shutdown and the latest comments from U.S. President Donald Trump. On Sunday, a compromise agreement was reached in the U.S. Senate between Democrats and Republicans to end the shutdown, which is boosting risk appetite. The document provides for restoring funding for government agencies through the end of January, while a decision on extending enhanced Affordable Care Act tax credits has not yet been made and will be put to a vote in December.

To fully resume government operations, the bill must be approved by the House of Representatives and signed by President Donald Trump, which will take some time. Additional support for prices comes from the White House pledge to pay at least $2,000 to every American—excluding high-income citizens—using revenues from tariffs, which could stimulate spending and support the economy. However, experts view Trump’s promises as populist, since the president cannot unilaterally authorize such payments and the issue has not been coordinated with Congress. Several estimates show that tariffs have brought the U.S. about $120.0 billion in revenue so far, while the proposal envisions outlays of $300.0 billion.

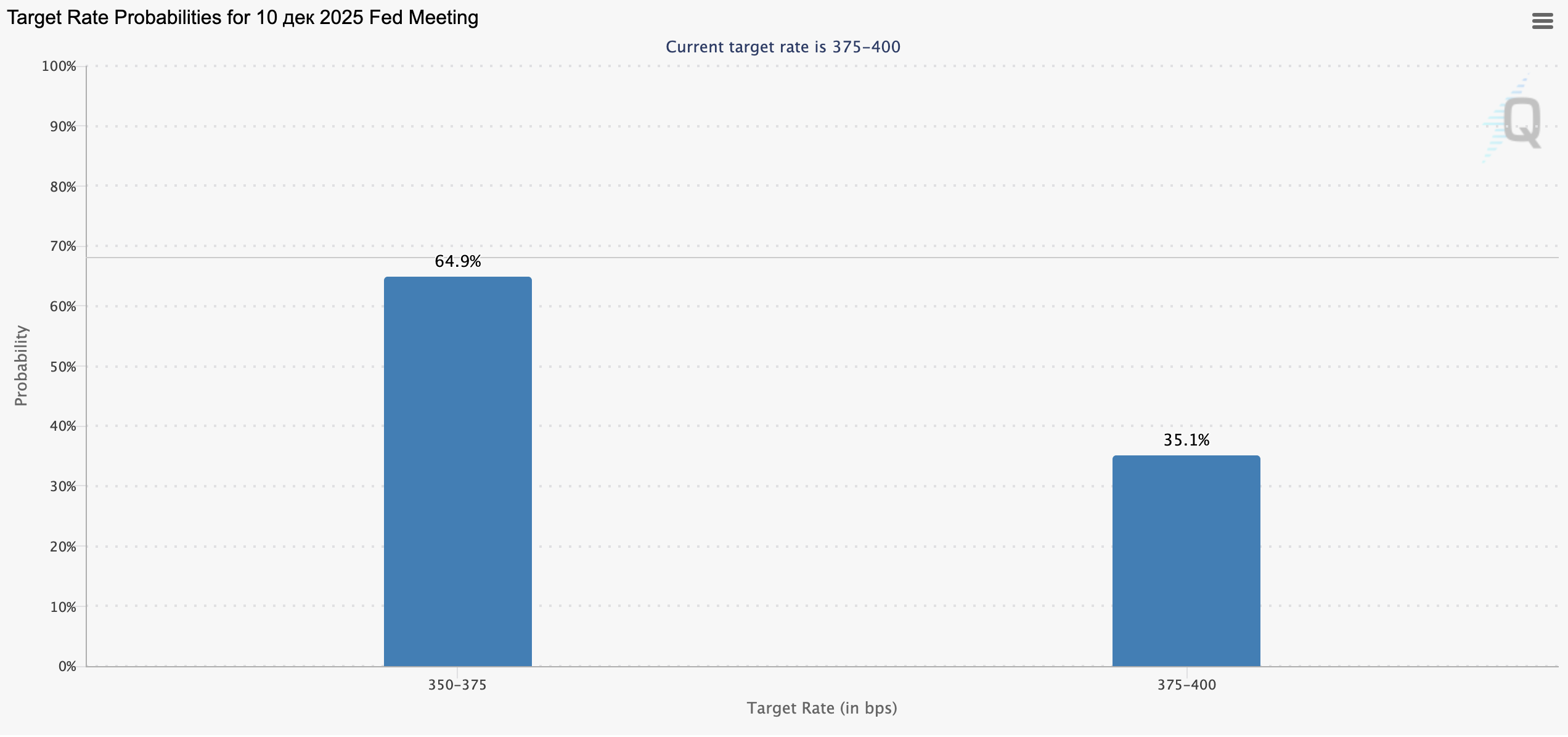

The chart shows market expectations for changes to the Fed’s key interest rate by the December 10, 2025 meeting (data: CME FedWatch Tool).

Market forecasts:

-

A 25 bp cut to a 3.50–3.75% range — probability 64.9%.

This is the base case, pointing to expectations of a dovish Fed stance.

-

Rate held at 3.75–4.00% — probability 35.1%.

This outcome is possible if inflation and the labor market remain resilient.

Interpretation:

Most investors expect the first rate cut since the Fed’s pause began. This signals a potential shift toward easier monetary policy, which typically puts pressure on the U.S. dollar and supports gold, equities, and cryptocurrencies.

Eurozone

The euro is strengthening today against the yen and the U.S. dollar but weakening versus the pound.

Eurozone Sentix investor confidence data released today showed the headline index fell from –5.4 points to –7.4 points in November versus an expected rise to –3.9, while the current situation gauge slipped from –16.0 to –17.5. Sentiment is deteriorating amid global trade uncertainty and geopolitical tensions, and experts believe the region’s economy will not return to recovery until next year. Meanwhile, European Central Bank (ECB) Vice President Luis de Guindos said policy rates are at appropriate levels, but adjustments are possible if needed.

United Kingdom

The pound is strengthening against the euro, the yen, and the U.S. dollar.

According to a survey by the Chartered Institute of Personnel and Development (CIPD), most employers plan to raise wages by 3.0% over the next 12 months, while one in six expects that the use of artificial intelligence (AI) will allow them to reduce headcount. On Tuesday at 09:00 (GMT+2), investors await September labor market data: forecasts point to unemployment rising from 4.8% to 4.9%, with employment growth slowing from 91,000 to 50,000—signals of cooling that would add to the case for Bank of England easing.

Japan

The yen is weakening against the euro, the pound, and the U.S. dollar.

Today’s Bank of Japan “Summary of Opinions” from its latest meeting indicated a growing need to raise interest rates in the near future, with some board members urging companies to continue wage indexation. Most experts expect a return to a more hawkish stance absent new global shocks. Despite this, the yen came under pressure from recent remarks by new Prime Minister Sanae Takaichi, who urged the BoJ not to rush tightening and to focus on achieving strong economic growth.

Australia

The Australian dollar is strengthening against the euro, the pound, the yen, and the U.S. dollar.

Investors and forex traders are assessing housing market data: in September, total building approvals rose from –3.6% to 12.0%, while approvals for private houses increased from –1.0% to 4.0%, confirming sector resilience amid global trade instability and raising the likelihood that the Reserve Bank of Australia (RBA) will refrain from further tightening.

Oil

The oil market is being pulled by opposing forces.

On the one hand, prices are supported by the prospect of a quick end to the U.S. government shutdown after 40 days—which would aid the economy and boost demand for crude—as well as LUKOIL’s force-majeure suspension of production at Iraq’s West Qurna-2 oil field. On the other hand, rising U.S. hydrocarbon inventories and the cancellation of 2,800 U.S. airline flights are raising concerns about jet fuel demand.