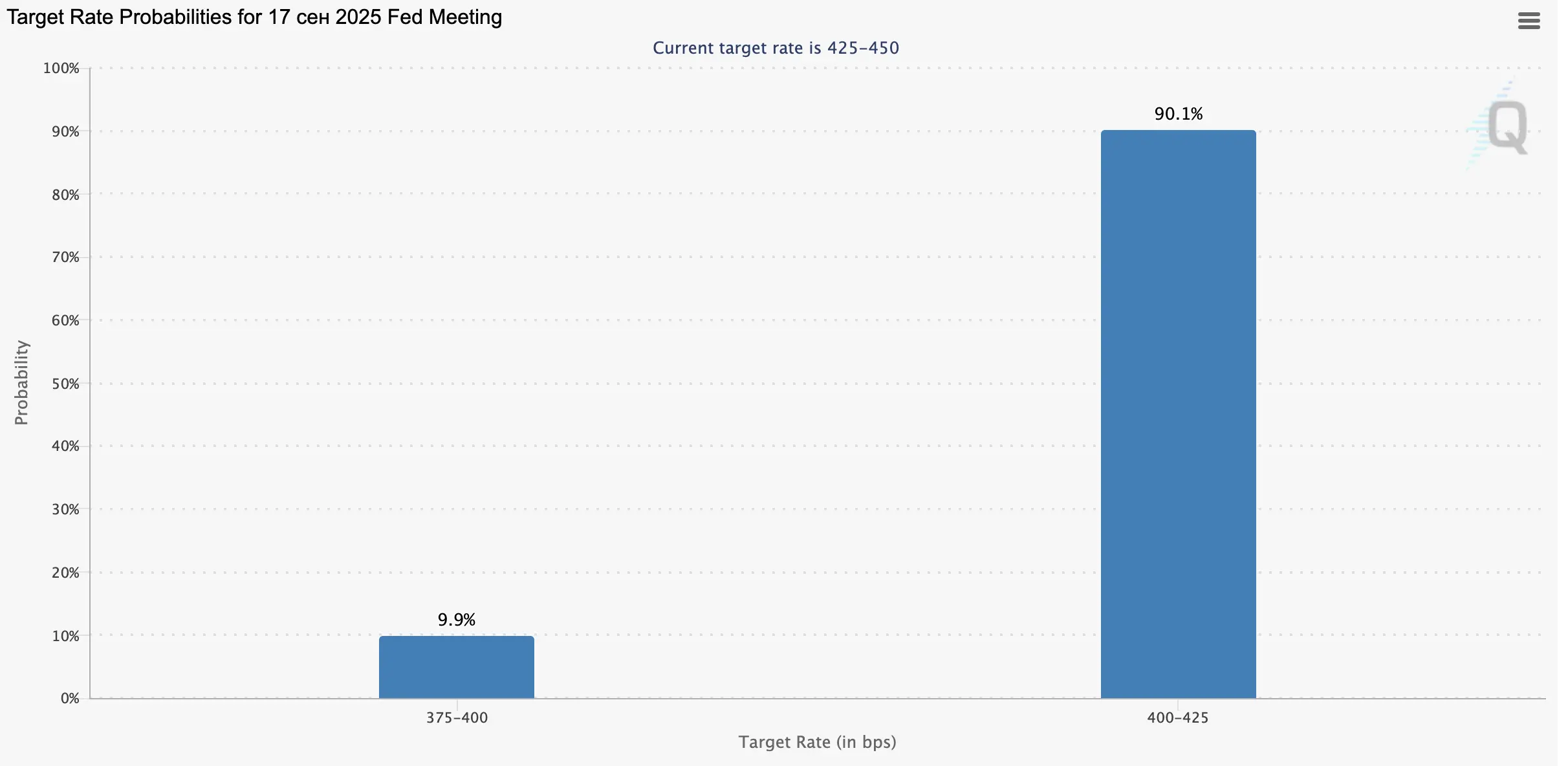

Revised labor market data covering the period from March last year to March this year showed a decrease of –911,000 jobs. Meanwhile, the Producer Price Index, scheduled for release today at 14:30 (GMT+2), is expected to remain at 3.3%. As a result, the probability of a 50-basis-point rate cut at the September 17 Fed meeting has decreased from 11.0% to 8.3%, according to the CME FedWatch Tool, supporting the US currency.

Eurozone

The euro is weakening against the dollar, the pound, and the yen.

Pressure on the currency is being driven by the political crisis in France as well as industrial production data. In July, French industrial output fell by –1.1% versus forecasts of –1.4%, underperforming the already weak results in Germany. At the same time, Spain reported a 2.5% increase and Italy 0.4%. Tomorrow at 14:15 (GMT+2), the European Central Bank (ECB) will announce its monetary policy decision. Analysts expect the key rate to remain at 2.15%, while investors will pay close attention to officials’ comments regarding borrowing costs for the remainder of the year.

United Kingdom

The pound is strengthening against the US dollar, euro, and yen.

The positive momentum is supported by stabilizing conditions in the domestic bond market. Despite speculation about a potential appeal to the IMF, analysts note that strong gold auction sales continue to provide support to the national economy. Meanwhile, the UK Treasury is preparing to issue mid-term bonds, with today’s auction set for £4.0 billion in six-year notes. Experts expect the current exchange rate of the pound to hold until next week’s Bank of England meeting, where policymakers are forecast to keep the interest rate at 4.00%.

Japan

The yen is gaining against the dollar and the euro but weakening versus the pound.

Political tensions following the resignation of Prime Minister Shigeru Ishiba on Sunday have eased, and investors are waiting for official government statements while assessing macroeconomic data and the domestic bond market. Household spending rose 5.1% year-over-year to 305,694 yen, while household income grew 1.0% to 701,283 yen. These figures reflect a stable upward trend, supporting Japan’s economic recovery in the second quarter.

Australia

The Australian dollar is strengthening against the pound, yen, euro, and the US dollar.

Traders are focused on July’s business performance report, which for the first time this year showed growth across all 13 key sectors of the economy, posting a combined increase of 2.9%. On a monthly basis, the strongest gains came from utilities (electricity, gas, and water) at 15.8%, professional, scientific, and technical services (4.6%), manufacturing (4.2%), and construction (3.8%). In annual terms, utilities led with 16.2%, followed by manufacturing (13.2%) and accommodation and food services (10.5%). Mining was the only sector to show a decline, down –1.7%.

Oil

Crude oil prices are rising, testing the 67.00 level.

Amid the decision by eight OPEC+ countries to exit voluntary production cuts in October, the US Energy Information Administration (EIA) revised its 2025 Brent crude price forecast upward from $67.22 to $67.80 per barrel, while maintaining expectations for a Q4 decline to $59.00. Analysts believe the supply glut triggered by OPEC+ will not be offset by India and China, both under pressure from the White House. Meanwhile, API data showed US fuel inventories rose modestly this week from 0.622 million barrels to 1.250 million. Investors now await the official EIA report at 16:30 (GMT+2).