In Germany, October factory orders showed an improvement: month-on-month growth accelerated from 1.1% to 1.5%, while analysts had expected 0.5%. Year-on-year, the indicator improved from –4.3% to –0.7%, still pointing to a challenging backdrop for domestic industry, which faces high import tariffs, elevated input costs, rising unemployment, and strong competition from Chinese producers. In France, October industrial production rose by 0.2% after a 0.7% gain in the previous month, beating the forecast of –0.3%.

At 12:00 (GMT+2), the euro area will release third-quarter GDP data. No changes are expected from the previous estimates of 0.2% q/q and 1.4% y/y, although there is a risk that the actual figures could come in slightly weaker given mounting headwinds in several sectors of the regional economy. Markets and forex traders will also focus on third-quarter employment data: preliminary projections point to a 0.1% increase q/q and 0.5% y/y.

For now, investors and forex traders have to rely on the October euro area retail sales report, which showed annual growth accelerating from 1.2% to 1.5% versus a 1.4% consensus, while the monthly reading slowed from 0.1% to 0.0%. In the US, at 15:30 (GMT+2), the personal consumption expenditures (PCE) price index will be published — a key gauge used by the Federal Reserve to assess underlying inflation trends and, therefore, potentially influencing next week’s rate decision. Forecasts suggest that the core PCE will rise 0.2% m/m and 2.9% y/y, while the broader headline index is expected to increase another 0.3% m/m, with the annual rate edging up from 2.7% to 2.8%.

GBP/USD

The pound is losing ground in the GBP/USD pair, testing the 1.3320 level on a downside break. Traders are taking profit on long positions after Wednesday’s strong rally and Thursday’s renewal of local highs from October 22. The US dollar has received a technical boost, but the fundamental backdrop has changed little: markets still anticipate monetary easing from the Federal Reserve at its December 9–10 meeting. Given recent soft macro data, Fed Chair Jerome Powell may also soften his tone on the pace of the rate-cut cycle. The Bank of England will meet on December 18, and consensus also points to a 25-basis-point cut.

At the same time, the Bank of England has so far failed to bring inflation risks under control, unlike the European Central Bank (ECB) and the Federal Reserve. Thursday’s UK macro data again highlighted the downturn in business activity: the S&P Global construction PMI for November fell from 44.1 to 39.4 points, while markets had expected 44.3 points. US releases, by contrast, looked moderately constructive: initial jobless claims for the week ending November 28 dropped from 218,000 to 191,000 versus a 220,000 forecast, and continuing claims eased from 1.943 million to 1.939 million. Factory orders in September slowed from 1.3% to 0.2%, below the 0.5% consensus.

AUD/USD

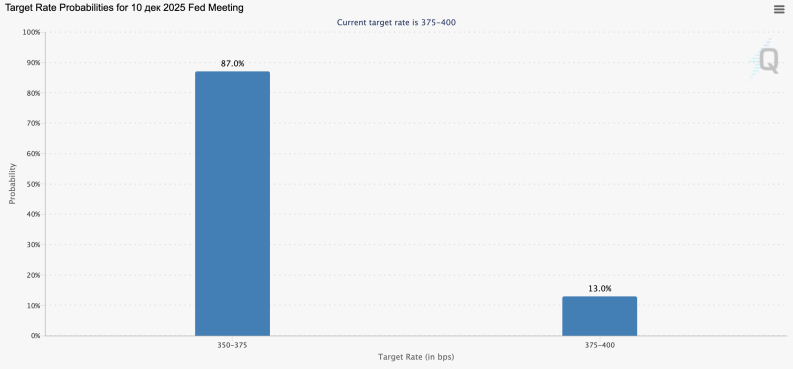

The Australian dollar is gaining against the US dollar in the AUD/USD pair, trading around 0.6621 and extending a solid short-term uptrend. The pair is set to end the week with a notable advance, updating local highs from October 7 amid expectations of a rate cut by the Federal Reserve next week. According to the CME Group FedWatch Tool, the probability of a 25-basis-point reduction to 3.75% is above 87.0%.

Markets will also be watching Fed Chair Jerome Powell’s speech. He may either hint at further policy easing or again emphasize a cautious, data-dependent approach focused on inflation risks. The US labor market report has been delayed by two weeks due to the government shutdown fallout, so today’s main focus at 15:30 (GMT+2) will be on the PCE price index. Forecasts call for core PCE to rise 0.2% m/m and 2.9% y/y, while the broader annual rate could pick up from 2.7% to 2.8%, signaling slightly higher inflation pressure.

September personal income and spending data are also due, with both indicators expected at 0.4% m/m. In Australia, Wednesday’s GDP release showed that third-quarter growth accelerated in annual terms from 1.8% to 2.1%, just shy of the 2.2% forecast, while quarterly growth slowed from 0.6% to 0.4% versus a 0.7% consensus. Trade figures were mixed: exports fell from 7.6% to 3.4%, imports rose from 1.8% to 2.0%, and the trade surplus widened from 3.707 billion to 4.385 billion Australian dollars. This kind of macro backdrop is likely to support an extended pause in the RBA’s monetary policy.

USD/JPY

The US dollar is losing ground against the yen in the USD/JPY pair, testing the 154.90 area and heading for a moderate weekly decline. The greenback remains under pressure as markets price in a Fed rate cut at the December 10 meeting. To a large degree this scenario is already reflected in current prices, and the key intrigue is whether Fed Chair Jerome Powell will soften his forward guidance on future policy steps. The Bank of Japan will meet on December 19, and investors still see a possibility of another tightening move.

Friday’s Japanese macro data were mixed. Household spending in October fell 2.9% after a 1.8% increase in September, while economists had expected a 1.0% decline. This may point to easing inflation pressures and could weaken expectations of a BoJ rate hike in December. At the same time, the leading index rose from 108.6 to 110.0 points, and the coincident index climbed from 114.6 to 115.4 points.

In the US, the PCE price index will also be released at 15:30 (GMT+2). As one of the Fed’s key inflation gauges, it can influence next week’s rate decision. Consensus calls for core PCE to rise 0.2% m/m and 2.9% y/y, while the broader index is expected to increase 0.3% m/m, with the annual rate edging up from 2.7% to 2.8%.

XAU/USD

The XAU/USD pair is edging higher, trading around 4226.25 and on track to finish the week roughly flat overall. Traders are reluctant to build new positions ahead of the December 9–10 Fed meeting. The CME Group FedWatch Tool assigns a probability of over 90.0% to a 25-basis-point cut in the federal funds rate to 3.75%, which would be a response to the latest weak macro data.

The November ADP employment report for the US private sector showed a drop of 32,000 jobs after a 47,000 increase in October, while markets had expected a modest 5,000 gain. However, Thursday’s jobless claims report painted a more constructive picture: initial jobless claims for the week ending November 28 fell from 218,000 to 191,000 versus a 220,000 forecast, and continuing claims slipped from 1.943 million to 1.939 million. Meanwhile, factory orders slowed from 1.3% to 0.2% in September, undershooting the 0.5% consensus.

Gold is also supported by expectations of monetary easing from the Bank of England and the Bank of Canada. Geopolitics remain another important driver: investors are closely watching the latest attempt at a peaceful resolution of the Russia–Ukraine conflict, initiated by US President Donald Trump.