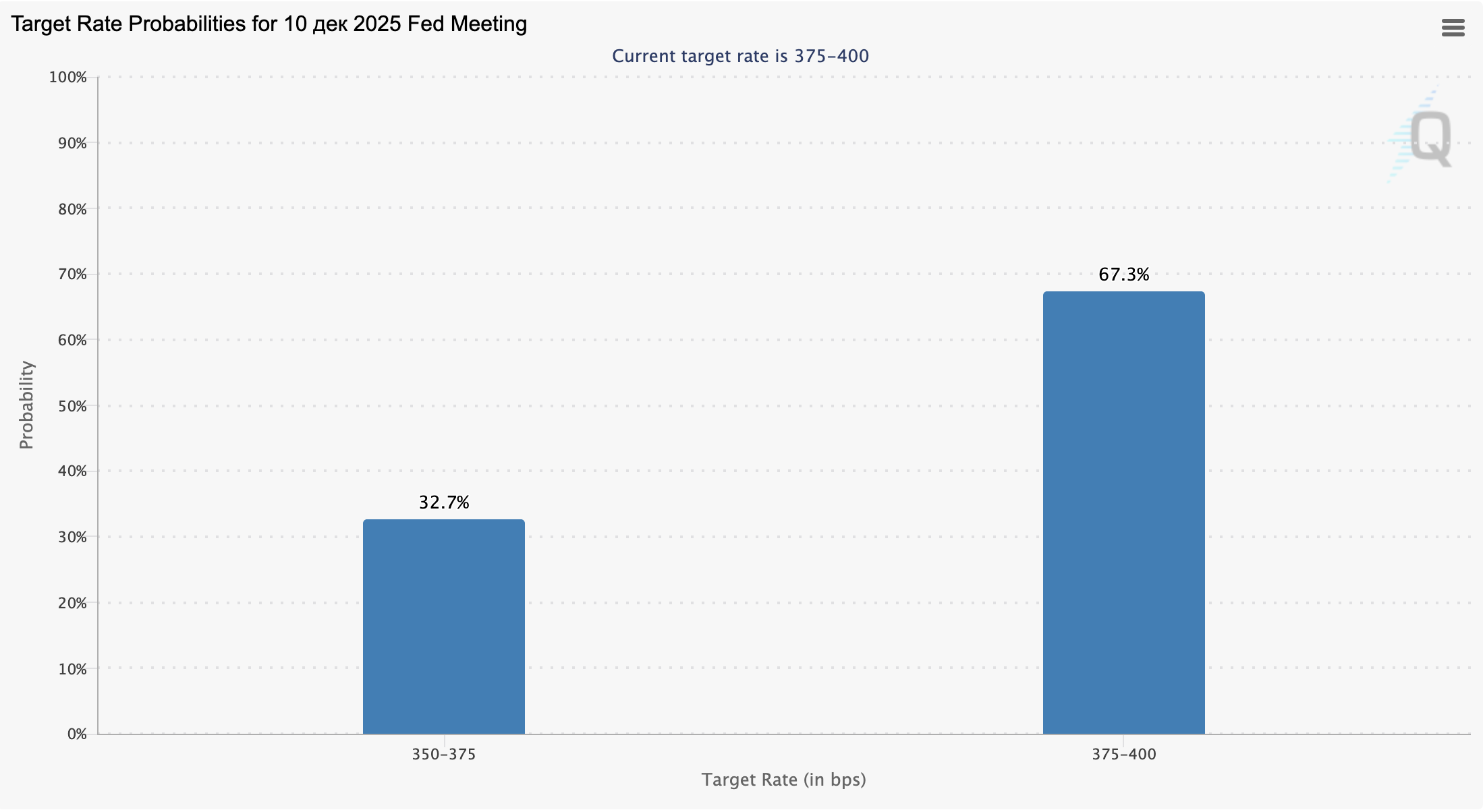

Forex traders are awaiting the minutes of the latest FOMC meeting, due at 19:00 GMT. The release may confirm Fed Chair Jerome Powell’s recent stance that policymakers need a pause in rate adjustments to assess the impact of previous measures. Based on recent comments, most officials — with the exception of Steven Miran, Christopher Waller and Michelle Bowman — appear to agree. However, the balance between hawks and doves on the Committee may shift after the release of September labour-market data tomorrow at 13:30 GMT. According to forecasts, unemployment is expected to remain at 4.3%, while nonfarm payrolls may rise from 22K to 50K, increasing the likelihood that borrowing costs will remain unchanged. At the same time, a cooling labour market would significantly influence the Fed’s communication.

Eurozone

The euro is strengthening against the yen and the pound, while trading mixed versus the US dollar.

Investors are focused on the October inflation report: headline CPI rose from 0.1% to 0.2% m/m and eased from 2.2% to 2.1% y/y. Core CPI increased from 0.1% to 0.3% m/m and stayed at 2.4% y/y — close to the ECB’s 2% target. These figures support expectations that the monetary-policy adjustment cycle is effectively over until the second half of next year. However, a rate cut remains possible if inflation falls below this threshold. Previously, ECB officials projected inflation at 2.1% in 2025 and 1.9% in 2026.

United Kingdom

The pound is weakening against the euro and the US dollar, while gaining versus the yen.

In October, headline CPI accelerated from 0.0% to 0.4% m/m and slowed from 3.8% to 3.6% y/y, slightly above market expectations of 3.5%. Core CPI rose from 0.0% to 0.3% m/m versus the expected 0.4% and eased from 3.5% to 3.4% y/y. According to the ONS, the softening of inflation was primarily driven by lower energy prices and reduced travel-related expenses, while food prices continued to rise — keeping overall inflation far above the Bank of England’s 2% target. Economists expect decisive action from the BoE at its December meeting following the government’s budget presentation, which includes tax adjustments that could weigh on domestic businesses.

Japan

The yen continues to weaken against the euro, the pound and the US dollar.

Traders reacted to Japan’s September core machinery orders, which rose from –0.9% to 4.2% m/m and reached 11.6% y/y (vs. the forecast of 5.4%). These figures indicate that the industrial sector is coping with the pressure from US trade tariffs. However, the data failed to support the yen, as markets remain focused on the diplomatic tensions with China. Beijing earlier advised its citizens to avoid travelling to Japan due to Tokyo’s position on the Taiwan issue — a move that could significantly hurt the tourism sector, which accounts for roughly 7% of Japan’s GDP and relies heavily on visitors from mainland China and Hong Kong (around 20% of all inbound arrivals). According to Nomura Research, a long-term boycott could result in annual losses of up to ¥2.2 trillion.

Australia

The Australian dollar is declining against the euro and the US dollar while showing mixed performance versus the yen and the pound.

Labour-market data increases the likelihood that the Reserve Bank of Australia will keep policy unchanged: in Q3, wage growth remained at 0.8% q/q and 3.4% y/y. Stronger wage gains in the public sector (3.8%) were offset by slower growth in the private sector (3.2%).

Oil

Oil prices are accelerating to the downside after the latest API report showed a 4.4 million-barrel increase in US crude inventories.

Traders are also cautious about Goldman Sachs’ outlook, which sees further downside in oil prices into late 2026. A sustained recovery and a return of Brent crude to around $70 per barrel would likely require new severe sanctions against Russia’s energy sector. At 15:30 GMT, markets expect the weekly EIA inventory data, which may show a 1.9 million-barrel draw.