Market activity remains restrained, as traders are in no hurry to open new positions and prefer to wait for the release of the final UK fourth-quarter gross domestic product (GDP) data. Preliminary estimates pointed to growth of 0.1% quarter-on-quarter and 1.0% year-on-year, but the actual figures could turn out to be significantly weaker.

The slowdown in activity in both manufacturing and services, recorded in January-February 2026, had already signaled a loss of positive momentum: the readings fell from 54.2 to 51.7 and from 55.0 to 52.4, respectively. Market participants are also reacting to the strengthening of the national currency, which has gained 2.3% against the US dollar since the beginning of March, potentially weighing on the United Kingdom’s export competitiveness.

Meanwhile, the main external economic factor remains the military conflict in the Middle East. Over the past month, the escalation has caused turbulence in commodity markets, and Brent Crude Oil prices have climbed from $86.5 per barrel at the beginning of the month to $97.2 at the opening of today’s session, while WTI Crude Oil is trading near $85.4 per barrel, creating a spread of $11.8. The blockade of the Strait of Hormuz is limiting about 20.0% of global exports, and the International Monetary Fund notes that the consequences may trigger a global but “asymmetric shock,” pushing energy prices higher and negatively affecting economic growth. The impact is expected to be especially severe for countries in Africa and Asia that are heavily dependent on imported crude oil, where access to supplies remains difficult even at elevated prices.

At the same time, low-income households are exposed to the highest risks, since food expenses account for around 36.0% of their budgets, compared with 20.0% in emerging markets and 9.0% in developed economies. Further increases in energy prices could intensify inflationary pressure in the eurozone and slow the UK’s economic recovery, especially in the transport and industrial production sectors, where fuel costs account for roughly 15.0–18.0% of production costs.

Against this backdrop, leading global regulators, including the Bank of England, are revising their expectations for future interest-rate adjustments. On March 19, members of the Monetary Policy Committee voted unanimously to keep borrowing costs at 3.75%, prompting most analysts to no longer rule out a hawkish cycle through the end of the year. At the same time, the US regulator left its parameters unchanged, maintaining the range at 3.50–3.75%, with only one participant — Board of Governors member Stephen Miran — supporting a cut. In the accompanying statement, officials for the first time since the start of the hostilities officially described the impact of the escalation on the US economy as “uncertain” and confirmed that they would continue to closely monitor the associated risks. The most important signal for long-term expectations came from updated macroeconomic forecasts: the regulator raised its 2026 core inflation projection to 2.7%, compared with 2.5% announced in December, effectively acknowledging the more persistent nature of price pressure.

According to statistics published yesterday, the number of approved mortgage loans in the UK rose by 62.58K against preliminary estimates of 61.00K, while the volume of such borrowing increased from £4.21 billion to £4.84 billion instead of the forecast £4.10 billion. Overall, the figure adjusted from £1.828 billion to £1.935 billion, compared with expectations of £1.600 billion. These data indicate that despite higher borrowing costs and uncertainty caused by the US-Iran confrontation, British households continue to borrow actively, supporting consumer activity. However, it should also be noted that February data do not yet reflect the sharp surge in energy-market prices observed throughout March.

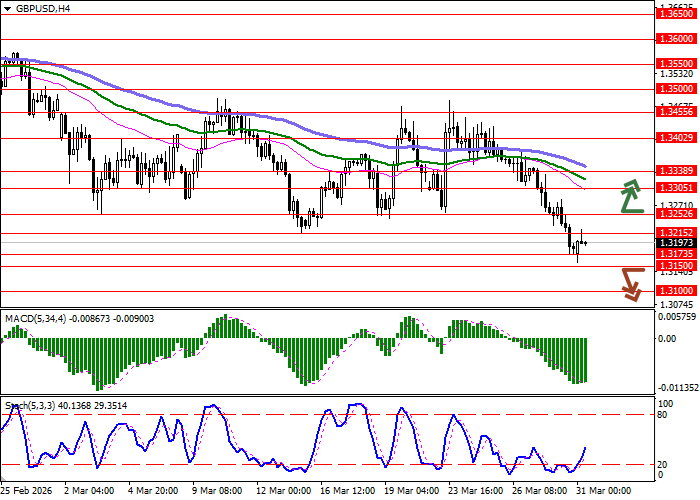

Support and resistance levels

On the daily chart, Bollinger Bands are showing a moderate decline. The price range is widening, but at the moment it is not fully keeping pace with the recent surge in bearish sentiment. MACD is declining, maintaining a firm bearish trend and remaining below the signal line. Stochastic is rapidly approaching its minimum levels, indicating risks of pound oversold conditions in the ultra-short term.

Resistance levels: 1.3215, 1.3252, 1.3305, 1.3338.

Support levels: 1.3173, 1.3150, 1.3100, 1.3037.

Trading scenarios and GBP/USD forecast

Short positions may be opened after a confident breakout below 1.3150 with a target at 1.3050. Stop-loss — 1.3200. Timeframe: 2–3 days.

A continuation of the corrective upward movement followed by a breakout above 1.3252 may become a signal to open long positions with a target at 1.3338. Stop-loss — 1.3215.

Scenario

| Timeframe | Intraday |

| Recommendation | SELL STOP |

| Entry point | 1.3145 |

| Take Profit | 1.3050 |

| Stop Loss | 1.3200 |

| Key levels | 1.3037, 1.3100, 1.3150, 1.3173, 1.3215, 1.3252, 1.3305, 1.3338 |

Alternative scenario

| Recommendation | BUY STOP |

| Entry point | 1.3255 |

| Take Profit | 1.3338 |

| Stop Loss | 1.3215 |

| Key levels | 1.3037, 1.3100, 1.3150, 1.3173, 1.3215, 1.3252, 1.3305, 1.3338 |