Early parliamentary elections are scheduled for February 8, called by Prime Minister Sanae Takaichi as she seeks to consolidate support from the ruling coalition ahead of large-scale fiscal reforms. The proposed package includes a temporary two-year suspension of the 8.0% consumption tax on food and non-alcoholic beverages, expanded social spending, and additional fiscal stimulus for households and businesses.

According to estimates, these measures could result in an annual budget shortfall of around ¥5.0 trillion (approximately $31.7 billion), against the backdrop of Japan’s already record-high public debt exceeding 230% of GDP. Looser fiscal policy combined with the Bank of Japan’s accommodative monetary stance has pushed 10-year government bond yields toward the 0.9–1.0% range, adding further pressure on the yen.

The situation has been exacerbated by mixed messaging from the prime minister regarding the exchange rate. Initial comments were interpreted by markets as tacit approval of further yen weakness to support exporters, which account for over 18% of GDP. However, subsequent attempts to emphasize currency stability were seen as poorly timed. Analysts note that this inconsistency has undermined efforts by Japan’s Ministry of Finance to curb devaluation expectations, triggering renewed selling of the yen, higher volatility, and additional stress in the bond market as fiscal risk premiums rise.

Meanwhile, the Bank of Japan remains cautious. Despite exiting negative interest rates and raising the policy rate to 0.75% in December, officials continue to warn against premature tightening. Recent inflation data from Tokyo showed annual CPI growth slowing to 1.5%, down from 2.3–2.5% at the end of 2025 and below the 2.0% target. This has reinforced expectations of a pause in the BoJ’s hawkish cycle, removing a key source of support for the yen.

At the same time, economic activity shows moderate expansion. The Jibun Bank services PMI edged up from 53.4 to 53.7 in January, beating expectations, while manufacturing activity held at 51.5.

The dollar, by contrast, remains attractive, reinforcing upward pressure on USD/JPY—especially after Kevin Warsh was named the leading candidate to become the next Federal Reserve chair in May. Markets interpreted this as a signal of policy continuity and a potentially firmer stance on inflation, easing concerns about political interference in monetary policy.

Additional support for the dollar comes from strong U.S. macro data. The producer price index rose 0.3% year-on-year in December, while the annual rate stood at 2.2%, confirming persistent cost pressures. Core inflation remains elevated, limiting the scope for early Fed easing. As a result, expectations for rate cuts have shifted toward a more gradual cycle focused on the second half of 2026, supporting Treasury yields and demand for dollar-denominated assets.

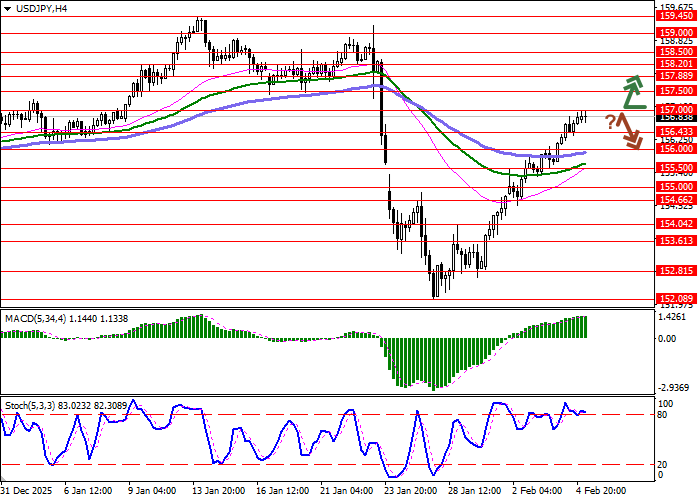

Support and resistance levels

On the daily chart, Bollinger Bands are attempting to flatten, with the price range narrowing and signaling mixed short-term momentum. MACD continues to rise, maintaining a strong buy signal above its signal line and approaching a potential breakout above the zero level.

The Stochastic oscillator has reached overbought territory and is moving sideways, indicating short-term risks of dollar overextension.

Resistance levels: 157.00, 157.50, 157.88, 158.20.

Support levels: 156.43, 156.00, 155.50, 155.00.

Trading scenarios and USD/JPY outlook

Long positions may be considered after a confident breakout above 157.00, targeting 158.20. Stop-loss: 156.43. Time horizon: 1–2 days.

A rebound from 157.00 as resistance followed by a break below 156.43 could open the way for short positions targeting 155.50. Stop-loss: 157.00.