German Minister for Economic Affairs and Energy Katherina Reiche, speaking at the international CERAWeek conference in Houston, highlighted growing risks for the country’s energy market amid the prolonged standoff between the United States and Iran, which has already triggered a sharp rise in gasoline, diesel, and aviation fuel prices. According to the ministry, the current situation has not yet led to a physical shortage, but if tensions persist, the likelihood of supply disruptions could rise significantly by late April to early May. This points to fragile supply chains and strong dependence on external factors. According to the German Economic Institute, prolonged high energy prices could lead to cumulative losses of up to €40.0 billion due to rising costs, increasing inflationary pressure and worsening conditions for the industrial sector. Germany’s economic recovery remains vulnerable amid declining corporate margins, weakening consumer demand, and rising stagflation risks, creating conditions for a potential revision of the European Central Bank’s monetary policy approach.

Economic data released this week also failed to support risk assets. Germany’s business expectations index fell to 86.0 points from 90.2 previously, matching forecasts, while the current conditions assessment reached 86.7 points, exceeding estimates of 86.0. The IFO business climate index, based on a survey of 7,000 executives across manufacturing, construction, wholesale, and retail sectors, declined from 88.4 to 86.4 points, although not as sharply as expected (86.2). Additionally, a 30-year bond auction held yesterday was sold at a yield of 3.420%, slightly below the previous 3.450%.

The overall situation in the debt market continues to limit demand for risk assets, as yields across major bonds remained in positive territory this week. On Tuesday, five-year bonds were sold at 2.720%, significantly above the previous 2.430%. Today, 12-month bonds are trading at 2.452% compared to 2.426%, while 10-year and 20-year yields stand at 2.953% and 3.367% versus 2.900% and 3.347%, respectively. Thirty-year bonds rose to 3.425%, above last Friday’s 3.391%.

Top gainers in the index include Siemens Energy AG (+4.55%), Infineon Technologies AG (+3.51%), Deutsche Bank AG (+3.22%), RWE AG (+3.19%), and Commerzbank AG (+3.02%).

Leading decliners include Deutsche Börse AG (–1.08%), SAP SE (–0.49%), Deutsche Telekom AG (–0.37%), Siemens Healthineers AG (–0.19%), and Deutsche Post AG (–0.36%).

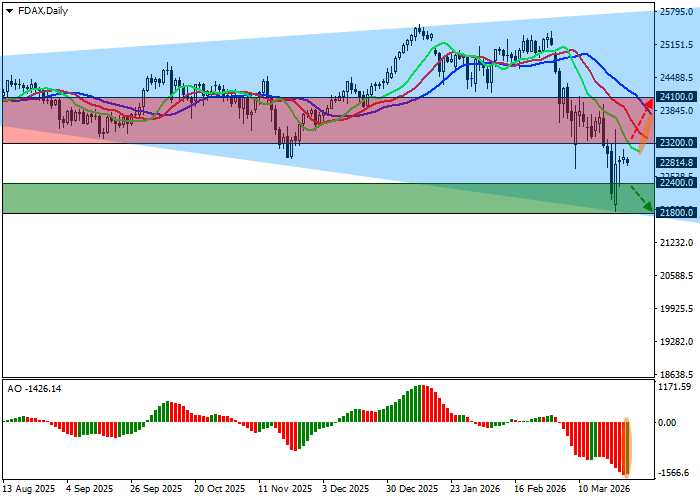

Support and resistance levels

On the daily chart, the instrument remains within a corrective trend, moving away again from the support line of the “expanding formation” pattern with boundaries at 26000.0–21500.0, which began forming early last year.

Technical indicators maintain a sell signal: fast EMAs on the Alligator indicator remain below the signal line, while the AO histogram forms corrective bars in the sell zone.

Support levels: 22400.0, 21800.0.

Resistance levels: 23200.0, 24100.0.

Trading scenarios and DAX 40 forecast

Short positions may be opened after consolidation below 22400.0 with a target at 21800.0. Stop-loss — 22800.0. Timeframe: 7 days or more.

Long positions may be opened after consolidation above 23200.0 with a target at 24100.0. Stop-loss — 22800.0.

Scenario

| Timeframe | Weekly |

| Recommendation | SELL STOP |

| Entry point | 22399.5 |

| Take Profit | 21800.0 |

| Stop Loss | 22800.0 |

| Key levels | 21800.0, 22400.0, 23200.0, 24100.0 |

Alternative scenario

| Recommendation | BUY STOP |

| Entry point | 23200.5 |

| Take Profit | 24100.0 |

| Stop Loss | 22800.0 |

| Key levels | 21800.0, 22400.0, 23200.0, 24100.0 |