Hawkish rhetoric from US President Donald Trump regarding readiness to launch a ground operation in Iran is increasing tensions and boosting volatility across global financial markets. Washington is considering strikes on key energy and oil infrastructure if Iranian authorities refuse to comply with a 15-point peace plan, which includes full control over the nuclear program and the transfer of approximately 450.0 kg of enriched uranium, signaling a shift toward direct military-strategic pressure. Additional escalation factors include the buildup of US military forces, including naval assets, as well as the deployment of transport and strike aircraft, amphibious capabilities, and tactical support units.

The current fundamental backdrop is interpreted by markets as a signal of potential disruption to hydrocarbon supplies. Reports that forces of the Ansar Allah movement have entered hostilities also heighten risks, as they may attempt to block the Bab el-Mandeb Strait, the second most important oil shipping route. In this case, crude oil and other goods would need to be transported around Africa, significantly increasing delivery times and causing sharp increases in shipping costs.

Under these conditions, capital is traditionally reallocated into safe-haven assets, including the US dollar, gold, and developed market government bonds, while emerging market currencies and the euro weaken. Regulators, including the US Federal Reserve, are likely to consider geopolitical risks as inflationary factors that limit room for monetary policy easing.

Regarding macroeconomic data, JOLTS job openings data will be released today at 16:00 (GMT+2), reflecting the number of new vacancies in the non-farm sector and serving as an important indicator of the US labor market. Analysts expect the figure to decline from 6.946 million to 6.900 million, potentially ending the positive trend that began in January after hitting a multi-year low of 6.542 million. Investors will also focus on the Conference Board consumer confidence index, which is expected to fall from 91.2 to 88.0 points in March.

Meanwhile, bond yields are rising actively. Benchmark 10-year securities are currently trading at 4.324%, slightly below 4.439% at the end of last week, while 20-year and 30-year yields stand at 4.902% and 4.893%, compared with 5.001% and 4.977%, respectively.

Top gainers in the index include Salesforce Inc. (+3.19%), The Travelers Co. (+2.30%), The Walt Disney Co. (+2.06%), and American Express Co. (+1.79%).

Among the biggest losers are Caterpillar Inc. (–4.02%), Cisco Systems Inc. (–3.60%), Nvidia Corp. (–1.40%), and Merck & Co., Inc. (–1.28%).

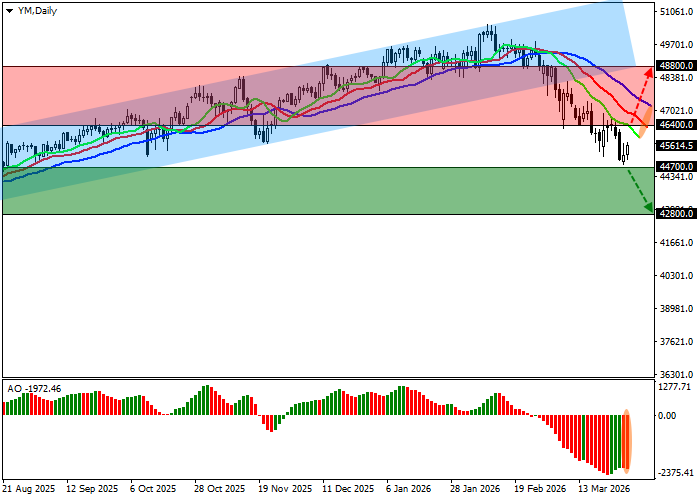

Support and resistance levels

On the daily chart, the instrument is declining again after an unsuccessful attempt to retest the support line of the 51,300.0–48,300.0 channel.

Technical indicators maintain a sell signal and continue to strengthen it, pointing to a stable downward trend. The EMA range of the Alligator indicator remains wide, while the AO histogram is forming new corrective bars below the transition level.

Support levels: 44,700.0, 42,800.0.

Resistance levels: 46,400.0, 48,800.0.

Trading scenarios and DJIA forecast

Short positions should be opened after consolidation below 44,700.0 with a target at 42,800.0. Stop-loss — 45,500.0. Implementation period: 7 days or more.

Long positions should be opened after consolidation above 46,400.0 with a target at 48,800.0 and stop-loss at 45,600.0.

Scenario

| Timeframe | Weekly |

| Recommendation | SELL STOP |

| Entry point | 44699.5 |

| Take Profit | 42800.0 |

| Stop Loss | 45500.0 |

| Key levels | 42800.0, 44700.0, 46400.0, 48800.0 |

Alternative scenario

| Recommendation | BUY STOP |

| Entry point | 46400.5 |

| Take Profit | 48800.0 |

| Stop Loss | 45600.0 |

| Key levels | 42800.0, 44700.0, 46400.0, 48800.0 |

Geopolitical risks and rising energy prices are becoming dominant drivers for equity markets. If inflation expectations continue to rise, the Federal Reserve may delay policy easing, increasing pressure on stocks. The Dow Jones remains vulnerable to further downside unless macroeconomic data improves.