Analysts expect a 25 basis point rate cut to 3.75%. According to the CME FedWatch Tool, the probability of such a scenario is estimated at 89.4% and has already been priced into the market. Recent macroeconomic data confirm further cooling in the labor market (U.S. employment fell by 32,000 in November according to Automatic Data Processing (ADP)) and declining inflationary pressure (the core Personal Consumption Expenditures (PCE) index slowed from 2.9% to 2.8% in September).

The upcoming rate decision is unlikely to be influenced by new macroeconomic data, although today at 17:00 (GMT+2) the market will receive updated JOLTS job openings statistics for September and October. These reports will reflect more current conditions, considering that the official U.S. Labor Department report was not published last Friday.

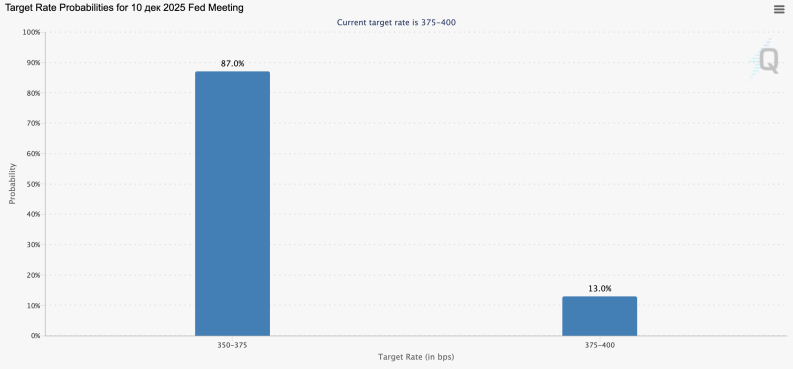

CME Group FedWatch Tool: the probability of a 25 bps cut to 3.75% exceeds 89%

CME Group FedWatch Tool: the probability of a 25 bps cut to 3.75% exceeds 89%

In the meantime, investors are focusing on recently updated data from the University of Michigan published on Friday: one-year inflation expectations were revised from 4.5% to 4.1%, and five-year expectations from 3.4% to 3.2%, increasing expectations for monetary easing. The euro also received support from Germany’s industrial production data: monthly activity accelerated from 1.1% to 1.8% in October (forecast: –0.4%), while annual growth moved from –1.0% to 0.8%.

The Sentix investor sentiment index for the euro area improved from –7.4 to –6.2 points, though it remains in negative territory. Investors are also awaiting data on Germany’s foreign trade, which showed slower export growth from 1.5% (revised from 1.4%) to 0.1% and a sharp decline in imports from 3.1% to –1.2%. As a result, the trade surplus widened from €15.3 billion to €16.9 billion (forecast: €15.2 billion).

GBP/USD

The British pound is gaining in the GBP/USD pair, trading around 1.3329 and extending a weak bullish impulse from the previous session. Market participants remain cautious ahead of the U.S. Federal Reserve decision, expecting a 25 bps rate cut to 3.75%. Although this outlook is largely priced in, traders will focus on comments from Fed Chair Jerome Powell, who may signal the continuation of monetary easing. Supporting this view are updated inflation expectations from the University of Michigan, which revised one-year forecasts to 4.1% and five-year forecasts to 3.2%. The latest PCE report also confirmed declining inflationary risks, with the core annual figure moderating to 2.8% and monthly values holding at 0.2%.

The market is also anticipating a potential rate cut from the Bank of England during its December 18 meeting. Unlike the U.S., inflation in the UK remains above target, yet the economy shows worrying signs of slowdown and labor market deterioration. The pound is additionally supported by confirmation of the UK national budget, which includes significant tax increases. The plan extends the lower tax bracket threshold for three more years (starting in 2028), expanding the number of taxpayers in higher brackets.

Furthermore, taxes on property, dividends, and savings will rise by 2%, and a new tax for electric vehicle owners will be introduced. These measures could generate an additional £26 billion annually, offsetting the current deficit of about £22 billion. Today’s focus includes retail sales data from the British Retail Consortium (BRC) for November, which declined from 1.5% to 1.2%, missing expectations of 2.4%.

AUD/USD

The Australian dollar is strengthening in the AUD/USD pair, recovering from the recent decline and testing the 0.6650 level, updating the September 18 high. The currency is supported by the results of the Reserve Bank of Australia (RBA) meeting, while traders also await the Federal Reserve decision scheduled for December 10 at 21:00 (GMT+2). The RBA kept rates unchanged at 3.60%, noting that recent inflation growth may be partially temporary, though some persistent trends remain. Economic activity continues to recover due to rising demand and investment.

The RBA also highlighted growing housing prices and a tense labor market, with employment continuing to decline throughout the past year. Traders additionally reacted to a drop in the National Australia Bank business confidence index, which fell from 6 to 1 point in November, while business conditions fell from 9 to 7 points. In the U.S., JOLTS job data will be published at 17:00 (GMT+2), helping substitute for missing labor statistics due to last Friday’s incomplete release.

Additional data include the NFIB Small Business Optimism Index at 13:00 (GMT+2), expected to rise from 98.2 to 98.4, and the Redbook retail sales index at 15:55 (GMT+2).

USD/JPY

The U.S. dollar is moderately strengthening against the Japanese yen, testing the 156.00 level to the upside. The pair continues to develop a bullish impulse as traders await the Federal Reserve decision due December 10 at 21:00 (GMT+2). Market participants largely expect a 25 bps cut to 3.75%, though Powell’s rhetoric remains key to understanding further monetary policy direction.

Additional support for the pair came from macroeconomic statistics from Japan, reducing expectations for monetary tightening by the Bank of Japan. Japan’s GDP contracted more than expected, falling from –0.4% to –0.6% quarterly and from –1.8% to –2.3% annually (forecast: –2.0%). Meanwhile, the GDP deflator rose sharply from 2.8% to 3.4%, signaling growing inflationary risks that may prompt future tightening. Today, investors assessed slower machinery and equipment orders, which rose 14.2% in December after a 16.8% increase previously.

XAU/USD

Gold prices are declining, with the XAU/USD pair testing the 4180.00 level to the downside. Market participants remain cautious ahead of the Fed meeting on December 10. According to the CME FedWatch Tool, the probability of a 25 bps cut stands at roughly 88%. Geopolitical tensions provide limited support for gold, with the Russia-Ukraine conflict still unresolved, lowering hopes for a near-term peace agreement.