Markets expect September unemployment to hold at 4.3%, while the US economy is forecast to add around 50K nonfarm payrolls. Average hourly earnings are projected to rise by 0.3% m/m and 3.7% y/y, potentially reinforcing expectations for further monetary easing from the Federal Reserve.

Traders are also assessing the minutes of the October FOMC meeting, which delivered mixed signals. Some policymakers believe further rate cuts will be appropriate “over time,” while others see no need for a December move. European investors, meanwhile, are watching October producer-price inflation: forecasts point to a –1.8% y/y decline after –1.7% previously (consensus –1.9%) and a modest rebound to 0.1% m/m after –0.1%. Earlier, eurozone CPI rose from 0.1% to 0.2% m/m and eased from 2.2% to 2.1% y/y. Later today at 15:00 GMT, November consumer-confidence data are expected to tick up from –14.2 to –14.0 points.

GBP/USD

The pound is under pressure in GBP/USD, testing 1.3050 to the downside during the Asian session. Activity remains subdued as US investors await the release of delayed September labour-market data at 13:30 GMT. Despite the shutdown, US lawmakers have approved temporary government funding through the end of January 2026, though political tensions remain elevated.

Traders are focused on the likelihood of further policy easing by the Federal Reserve. Only about half of analysts currently expect a 25 bp rate cut to 3.75% in December, with incoming data likely to be decisive. In contrast, expectations for a Bank of England cut are more pronounced due to easing inflation and softer domestic growth. Yesterday’s UK data confirmed this trend: core CPI slowed from 3.5% to 3.4% y/y, headline inflation eased from 3.8% to 3.6% y/y, and monthly CPI rose from 0.0% to 0.4%, driven by lower energy and travel costs. Notably, retail-price inflation slowed from 4.5% to 4.3% y/y.

AUD/USD

The Australian dollar is recovering in AUD/USD after yesterday’s sharp drop, which pushed the pair to fresh lows last seen on October 17. Support came from the latest PBoC meeting, where China’s central bank kept its benchmark rate unchanged at 3.00%, noting that additional stimulus is not urgently required despite mixed domestic data on consumption and industrial output.

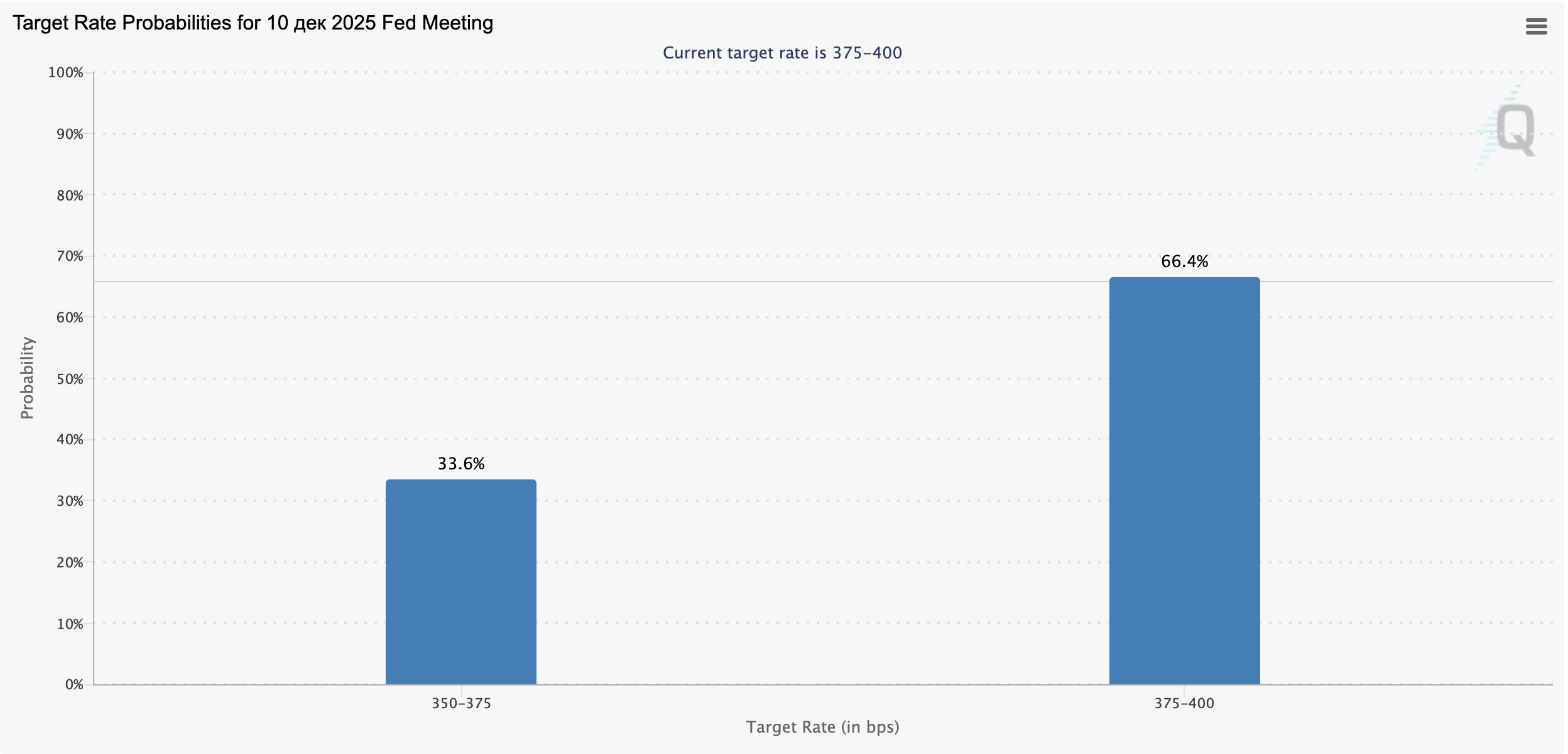

In addition, many traders are covering short positions ahead of today’s delayed US labour-market release at 13:30 GMT. Forecasts call for roughly 50K new jobs after 22K previously, unemployment at 4.3%, and wage growth at 0.3% m/m and 3.7% y/y. These figures may significantly influence the Fed’s December rate decision. According to the CME FedWatch Tool, only 33% of analysts expect a –25 bp move to 3.75%. In Australia, S&P Global will release November PMI data on Friday at 22:00 GMT.

USD/JPY

The US dollar is posting moderate gains in USD/JPY, testing 157.50 and refreshing mid-January highs. Support comes from expectations surrounding today’s delayed US labour-market report at 13:30 GMT — a key driver for determining whether the Fed cuts rates in December.

The next FOMC meeting is scheduled for early December, with roughly half of analysts expecting a 25 bp cut. Yesterday’s minutes from the October meeting, where rates were lowered to 4.00%, revealed divided views: most policymakers favour further easing but only when warranted by data. Japanese traders will watch Friday’s inflation release at 23:30 GMT, with core CPI expected to rise from 2.9% to 3.0%, which may support arguments for a more restrictive BoJ stance.

XAU/USD

Gold is consolidating near 4065.00 as traders await the delayed US labour-market figures at 13:30 GMT. Markets expect unemployment to remain at 4.3% and job growth near 50K, with wage gains of 0.3% m/m and 3.7% y/y, reinforcing expectations for further Fed easing. Additional support for gold comes from persistent geopolitical tensions and the prospect of monetary easing by the Bank of England, Bank of Canada, and other major central banks.