Forex traders are assessing the outcome of the Federal Reserve meeting, where officials cut the interest rate by 25 basis points to 3.75–4.00% and announced the end of the quantitative tightening (QT) program as of December 1. During the press conference, Fed Chair Jerome Powell said the regulator might pause further monetary easing to evaluate economic data, causing December rate-cut expectations to drop from 90.0% to 67.0%, according to the CME FedWatch Tool.

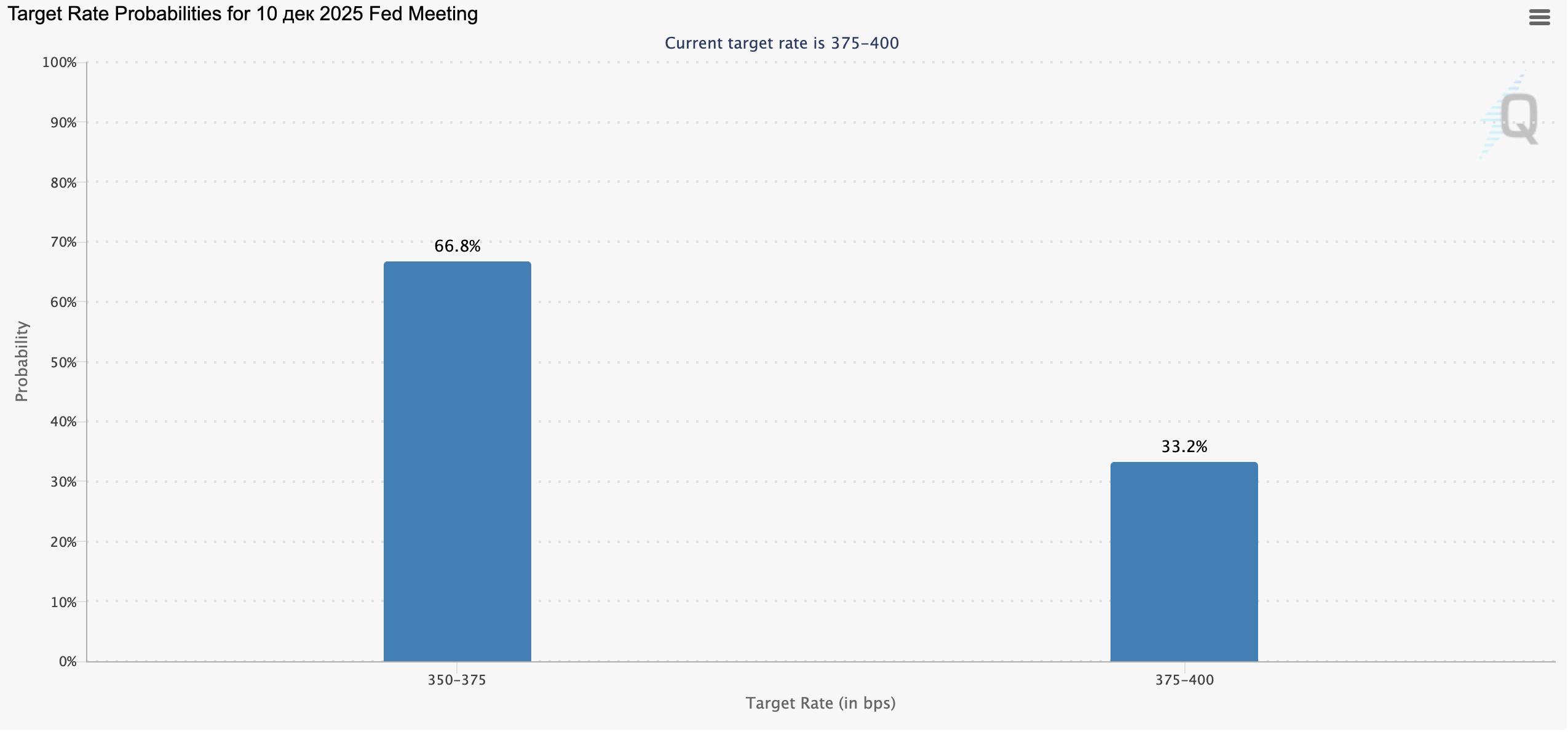

Fed rate-change probabilities per CME FedWatch Tool for the December 10, 2025 meeting: 66.8% for a cut to 3.50–3.75%, and 33.2% for maintaining 3.75–4.00%.

Today, Kansas City Fed President Jeffrey Schmid — the only official opposing the rate cut — stated that inflationary pressure may continue to rise, contradicting the Fed’s 2.0% target. He added that the labor market slowdown is due to structural changes in technology and demographics, not demand weakness, suggesting that a dovish stance may fail to sustain growth.

Eurozone

The euro is weakening against the U.S. dollar, strengthening versus the pound, and showing mixed movement against the yen.

Forex traders are focused on preliminary EU inflation data: in October, the consumer price index rose from 0.1% to 0.2% month-over-month and slowed from 2.2% to 2.1% year-over-year, matching forecasts. The core CPI increased from 0.1% to 0.3% monthly and remained steady at 2.4% annually, above the 2.3% estimate. The services sector saw the strongest acceleration — up to 3.4%. With inflation still slightly above the ECB’s target, most analysts believe the regulator will likely keep rates unchanged until mid-2026, with a roughly 60.0% probability. Meanwhile, Bank of France Governor François Villeroy de Galhau emphasized that the ECB should retain flexibility to adjust policy in response to market shifts. German retail sales rose by 0.2% month-on-month and year-on-year in September, reversing declines of –0.5% and –1.6%, respectively.

United Kingdom

The pound is weakening against the euro, U.S. dollar, and yen.

Nationwide Building Society reported that UK house prices rose 2.4% year-over-year in October, up from 2.2% and beating expectations of 2.3%. Monthly growth slowed slightly from 0.5% to 0.3%. The housing market remains stable despite weaker consumer confidence and early signs of labor market cooling. Analysts note that demand could rebound if the Bank of England loosens monetary policy soon.

Japan

The yen is strengthening against the pound while trading mixed versus the euro and dollar.

Investors are assessing Tokyo’s inflation data: both headline and core CPI rose from 2.5% to 2.8% year-over-year in October, surpassing the Bank of Japan’s 2.0% target. Industrial production rebounded from –1.5% to 2.2%, beating forecasts of 1.5%, while retail sales increased from –0.9% to 0.5% versus expectations of 0.8%. These figures support potential policy tightening, though officials remain cautious that Prime Minister Sanae Takaichi’s government may resist a hawkish shift.

Australia

The Australian dollar is weakening against the yen and U.S. dollar but strengthening against the euro and pound.

Investors are focused on wholesale inflation data: in Q3, the Producer Price Index rose from 0.7% to 1.0% quarter-over-quarter, exceeding the 0.8% forecast, and from 3.4% to 3.5% year-over-year — above the Reserve Bank of Australia’s 2.0–3.0% target range, limiting policy easing prospects. A Reuters survey shows most economists expect the RBA to hold rates at 3.60% through year-end.

Oil

Oil prices are moderately rising, supported by several counterbalancing factors. On one hand, the U.S.–China de-escalation following the meeting between Presidents Donald Trump and Xi Jinping eased global recession risks, boosting energy demand.

On the other hand, Saudi Arabia — the world’s largest crude exporter — may cut the Arab Light price for Asian buyers to a multi-month low of $1.20–1.50 per barrel, limiting the upside momentum for “black gold.”