Forex today: the dollar under pressure from Fed commentary

Investors and forex traders are focused on remarks from Federal Reserve officials confirming the likelihood of a November pause in the dovish cycle. St. Louis Fed President Alberto Musalem said October’s rate cut was needed to support the labor market, but inflation remains elevated and borrowing costs are nearing neutral, warranting a wait-and-see stance. Cleveland Fed President Beth Hammack added that the current level of consumer prices argues against further policy easing. By contrast, Chicago Fed’s Austan Goolsbee stressed that, with official statistics limited by the shutdown, caution is needed around rate adjustments. Meanwhile, President Donald Trump told reporters at the White House that trade talks with India are going well and that New Delhi has largely halted purchases of Russian oil. He also said he plans to visit India in 2026.

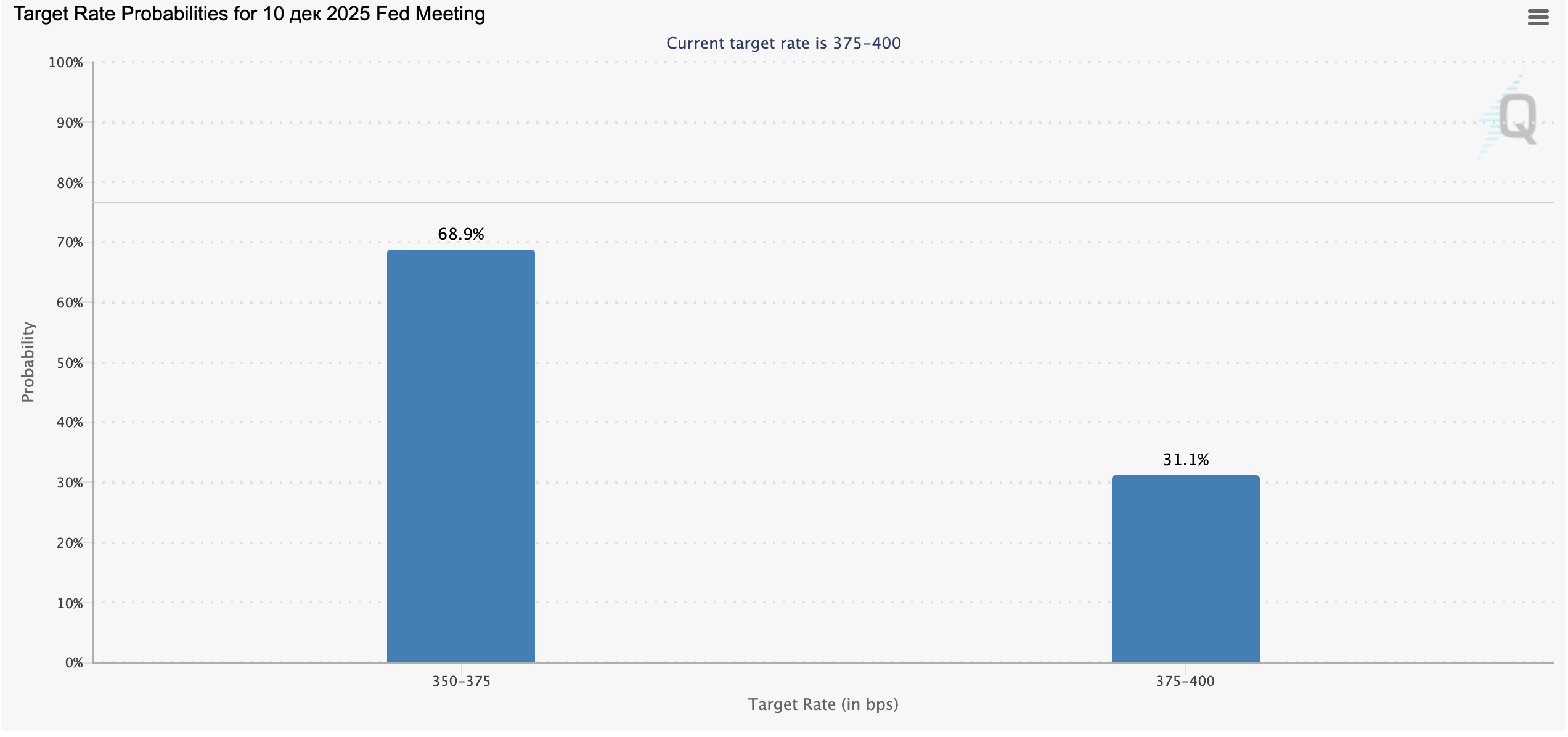

The chart shows market expectations for changes to the Fed policy rate for the 10 December 2025 meeting (CME FedWatch Tool).

Current target rate: 3.75–4.00%.

Market projections:

-

A 25 bps cut to 3.50–3.75% — probability 68.9%.

This is the base case, reflecting expectations for Fed policy easing by year-end.

-

No change (3.75–4.00%) — probability 31.1%.

Less likely, but possible if inflation and the labor market prove resilient.

Interpretation:

Most participants are pricing in the first rate cut since the pause began. That points to a likely shift toward a looser policy stance, which typically pressures the US dollar and supports equities, gold, and cryptocurrencies.

Eurozone

The euro is strengthening against the pound, yen, and US dollar.

Germany’s September trade data showed exports rising from −0.5% to 1.4% m/m and imports from −1.4% to 3.1% m/m, narrowing the trade surplus from €16.9 bn to €15.3 bn. While firms are successfully shifting away from the US toward other markets, the outlook remains cautious: the German chamber DIHK expects GDP to stagnate this year and grow 0.7% next year, whereas government projections imply −0.2% in 2025 and +1.3% in 2026.

United Kingdom

The pound is weaker versus the euro and the US dollar, and mixed against the yen.

Investors and forex traders are assessing house-price data from major mortgage lender Halifax Bank Plc.: in October prices rose 0.6% m/m vs. 0.1% expected and 1.9% y/y vs. 1.5%. Analysts note some households plan to buy soon amid worries about finances after the budget, which, according to The Times, may include an income-tax increase previously flagged by Chancellor Rachel Reeves: the rate would rise by two pence while National Insurance contributions fall by the same amount, shifting the burden from workers toward groups such as pensioners and landlords.

Japan

The yen is weaker against the euro and mixed versus the US dollar and the pound.

Household spending for September fell to −0.7% m/m (from 0.6%) and to 1.8% y/y (from 2.3%), below the 2.5% consensus and the Bank of Japan’s 2.0% target, which will factor into policy prospects. A Reuters survey of economists suggests real GDP could contract 2.5% q/q in Q3 after +2.2%, reflecting pressure from US trade tariffs.

Australia

The Australian dollar is weaker against the euro but firmer versus the pound, yen, and the US dollar.

With few major releases ahead, expectations that the Reserve Bank of Australia will keep policy steady are supporting the currency. On Tuesday the RBA held the cash rate at 3.60% and signaled caution on further easing amid high inflation, stronger-than-assumed consumer demand, and a recovering construction market. At the follow-up press conference Governor Adrian Orr said “there may be no more rate cuts.”

Oil

Crude prices are making a moderate attempt to rise on expectations of a meeting between US President Donald Trump and Hungary’s Prime Minister Viktor Orbán, where the White House is expected to push Budapest to stop buying Russian energy—potentially boosting demand for other producers’ oil and supporting prices.

Even so, the fundamental backdrop remains soft: fuel inventories rose by 6.5 million barrels on the week, according to the American Petroleum Institute (API), and by 5.202 million barrels per the US Energy Information Administration (EIA). A firmer US dollar—helped by the Fed holding rates—continues to pressure alternative assets, including commodities.