Forex Market Overview and U.S. Dollar Dynamics

Forex investors are focused on comments from Federal Reserve officials highlighting uncertainty about future monetary policy steps. Last week, Fed Chair Jerome Powell stated that another rate cut in December is not predetermined, noting that the institution sees growing confidence in pausing to assess the impact of recent decisions. This disappointed traders, who reduced the probability of another rate adjustment next month from 90.0% to 67.0%. However, not all Fed officials share Powell’s stance. FOMC member Lisa Cook warned that keeping borrowing costs high increases the risk of a sharp deterioration in the labor market, even though current conditions remain stable.

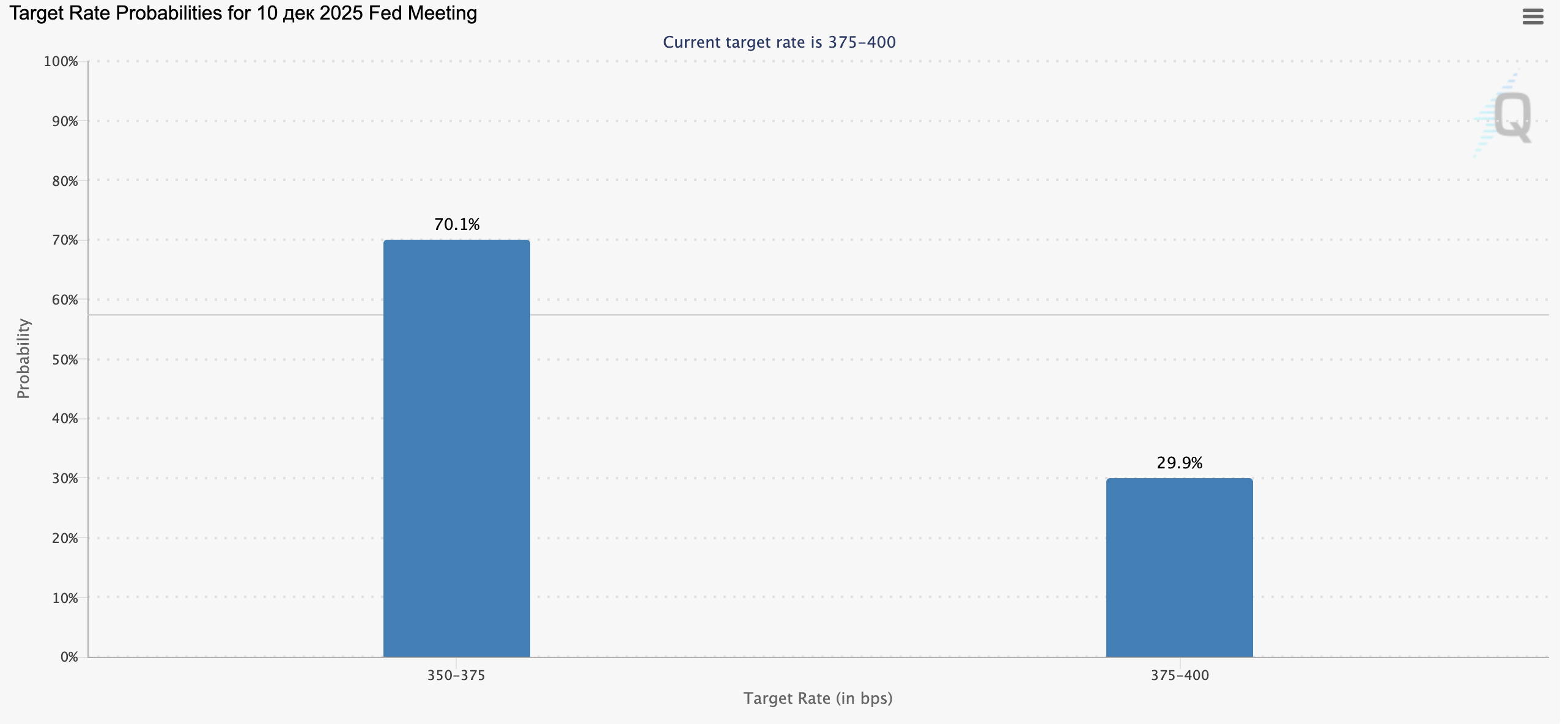

Chart: Market expectations for the Fed rate decision on December 10, 2026, according to CME FedWatch Tool.

Current rate range: 3.75–4.00%

According to the latest data:

- 70.1% of market participants expect a cut to 3.50–3.75%.

- 29.9% believe the rate will remain unchanged.

After the latest 25-basis-point rate cut, market expectations shifted toward further monetary easing by year-end. Against this backdrop, the U.S. Dollar Index rose by 0.8%, pressuring risk assets such as tech stocks and cryptocurrencies as investors moved capital into U.S. Treasuries.

Meanwhile, excessive rate reductions could influence inflation expectations. According to Cook, both risks must be considered at the December meeting. San Francisco Fed President Mary Daly echoed this, emphasizing that future steps should balance inflation and employment risks. Board member Steven Miran told Bloomberg that the rebound in equity and credit markets isn’t a sign of overly loose policy, advocating for a continued dovish approach. In contrast, Kansas City Fed’s Jeffrey Schmid, Dallas Fed’s Lorie Logan, Cleveland Fed’s Beth Hammack, and Chicago Fed’s Austan Goolsbee favor a more hawkish stance, noting that inflation remains well above the 2.0% target and could accelerate toward year-end.

Eurozoneс

The euro is losing value against the U.S. dollar and yen but strengthening versus the pound. Germany’s foreign trade report from GTAI forecasts a record deficit of €87.0 billion in trade with China by year-end, driven by higher U.S. tariffs. The agency projects an 11% drop in German exports to China and a surge in imports, as Beijing seeks new export markets. This imbalance may further weigh on the euro and the broader EU economy.

United Kingdom

The pound is weakening against major rivals — the euro, U.S. dollar, and yen. Forex traders are focused on Chancellor Rachel Reeves’ comments outlining anti-inflation measures and the goal of lowering interest rates to support growth. Economists expect the new budget, due November 26, to include significant tax hikes — possibly raising personal income and VAT rates by £26–30 billion — putting additional pressure on domestic businesses.

Japan

The yen is gaining against major currencies — the euro, dollar, and pound. The move followed Finance Minister Satsuki Katayama’s remarks that the government is closely monitoring currency movements for speculative activity. Such statements are often interpreted as a warning of potential interventions to stabilize the yen. However, the correction remains limited by weak October manufacturing data — the PMI fell to 48.2, its lowest in 19 months — increasing recession risks and reducing the likelihood of continued hawkish policy.

Australia — RBA’s Policy and Australian Dollar Dynamics on Forex

The Australian dollar is falling against all major counterparts — the euro, pound, yen, and U.S. dollar. At its latest meeting, the Reserve Bank of Australia (RBA) kept rates unchanged at 3.60%, citing persistent inflation and stronger-than-expected consumer demand. Governor Michele Bullock stated that further cuts “may no longer be appropriate.” Inflation forecasts were revised upward: headline CPI is expected to reach 3.2% by year-end, and core inflation is not projected to return to the 2.0–3.0% target before 2027.

Oil Market and Forex Correlation — Brent Prices Under Pressure

Oil prices are moving lower, pressured by OPEC+’s decision to increase production by another 137,000 barrels per day in December. Meanwhile, Morgan Stanley raised its forecast for Brent crude in H1 2026 from $57.50 to $60.00 per barrel. Later today (23:30 GMT+2), the American Petroleum Institute (API) will release inventory data; last week’s 4-million-barrel drawdown, if repeated, could lend short-term support to oil prices and the petrocurrencies linked to them.