Investor focus remains on the probability of a Federal Reserve rate cut in December, which — according to the CME FedWatch Tool — has slipped from 60.0% to 49.9%. Openly dovish rhetoric now comes only from Steven Miran, appointed by President Donald Trump, and partially from Christopher Waller and Michelle Bowman. Other FOMC members remain cautious, unsure whether inflation has cooled enough, while Boston Fed President Susan Collins — who previously advocated monetary easing — has shifted toward the hawkish camp. Analysts do not rule out a 25-basis-point cut at the next meeting, but note that any such move would likely be followed by a pause early next year to assess the effects.

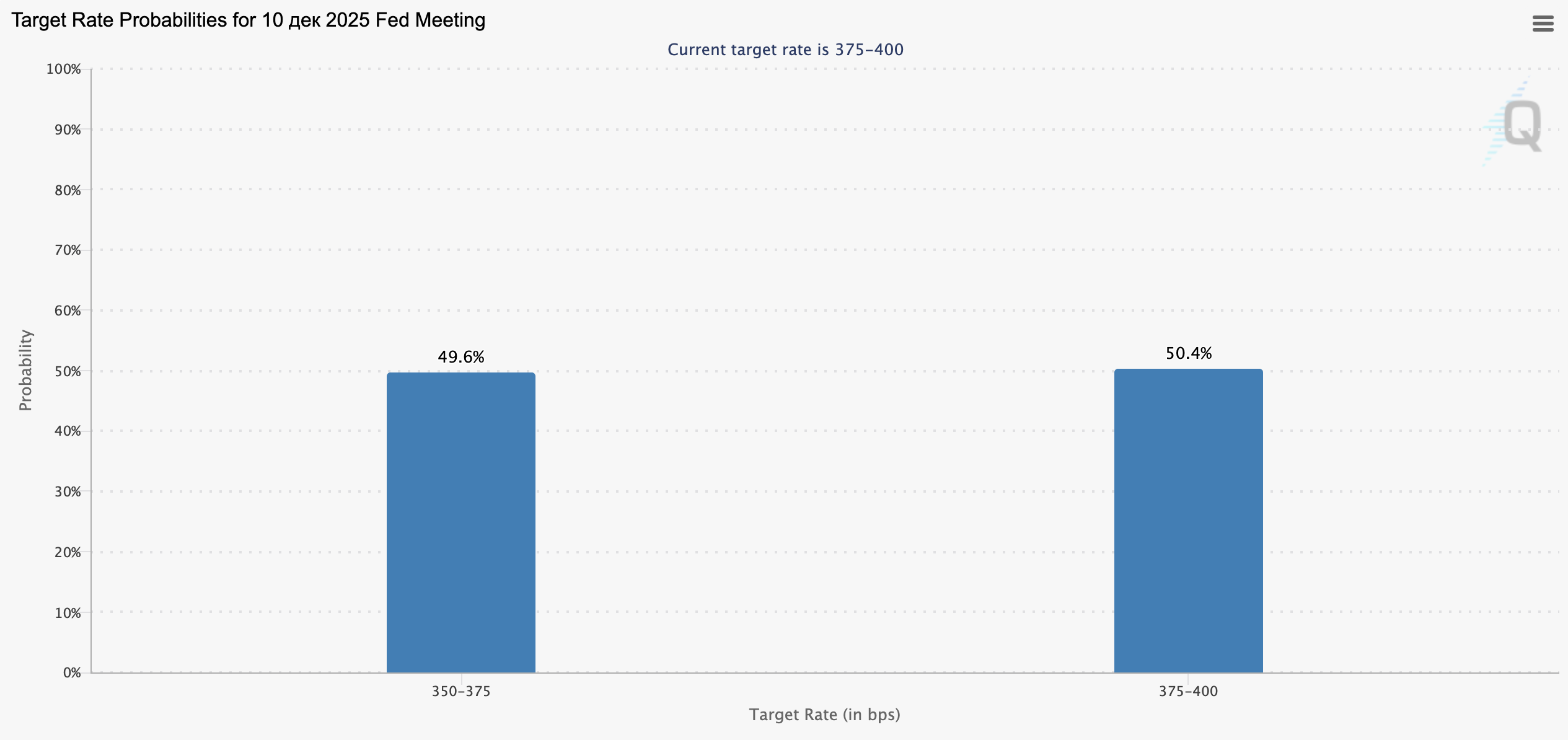

The chart shows market expectations for the Fed meeting on December 10, 2026. Traders are almost evenly split:

- 49.6% expect a rate cut to 3.50–3.75%

- 50.4% expect the rate to remain unchanged at 3.75–4.00%

This distribution signals that the market has no clear consensus. Investors and forex traders are waiting for fresh inflation and labor-market data before placing confident bets on the Fed’s next move.

Eurozone

The euro is weakening against the yen and shows mixed dynamics against the US dollar and the pound.

Today, the EU released preliminary GDP data: in the third quarter, the indicator rose from 0.1% to 0.2% quarter-on-quarter, in line with forecasts, and from 1.5% to 1.4% year-on-year, slightly above expectations of 1.3%. This suggests that the eurozone economy continues to recover even under pressure from higher US tariffs, making a near-term policy shift by the European Central Bank (ECB) unlikely. Meanwhile, ECB Executive Board member Claudia Buch warned that financial markets underestimate geopolitical risks, which affect almost all banks in the euro area to some degree, and that loosening regulatory requirements now could destabilize the sector over the long term.

United Kingdom

The pound is weakening against the yen and shows mixed performance in pairs with the US dollar and the euro.

Today, UK government bond yields rose sharply after reports that Chancellor Rachel Reeves no longer plans to raise income tax in the Autumn Budget, which will be presented on November 26. The yield on 10-year gilts jumped by around 12 basis points early in the session before easing to 4.51%, while yields on 20- and 30-year bonds increased by 8.5 and 9.0 basis points, respectively. Analysts now expect the £30 billion budget gap to be filled through changes to a range of smaller taxes.

Japan

The yen is strengthening against the euro, the pound, and the US dollar.

On Monday at 01:50 (GMT+2), Japan will publish preliminary GDP figures. In the third quarter, growth is expected to slow from 0.5% to 0.4% quarter-on-quarter and from 2.2% to 2.0% year-on-year, pressured by higher US tariffs — a factor that increases the likelihood that the Bank of Japan will keep interest rates unchanged, weighing on the yen in the medium term. However, industrial production data, due at 06:30 (GMT+2), is expected to show a rebound in September from –1.5% to 2.2%.

Australia

The Australian dollar is weakening against the euro, the pound, and the yen, while showing mixed dynamics in the pair with the US dollar.

Sentiment is being hurt by weak macroeconomic data from China, Australia’s largest trading partner. In October, China’s industrial production slowed from 6.5% to 4.9% year-on-year versus expectations of 5.5%, fixed-asset investment fell by 1.7% versus a projected decline of 0.9%, and retail sales eased from 3.0% to 2.9%. Cooling economic activity in China could negatively affect trade volumes with Australia and add further pressure on the AUD.

Oil

Initial gains in oil prices have reversed, with the market reacting to opposing factors.

On the one hand, prices are supported by concerns over possible disruptions to Russian crude exports after the port of Novorossiysk suspended operations due to partial terminal damage. On the other hand, bullish momentum is limited by US Energy Information Administration (EIA) data showing a 6.413 million-barrel increase in fuel inventories for the week, compared with expectations of a 1.000 million-barrel build. Gasoline stocks fell by just 0.945 million barrels versus a forecast decline of 1.900 million barrels, while distillate inventories dropped by 0.637 million barrels versus an expected 2.000 million-barrel draw.