On Wednesday at 16:45 (GMT+2), the Federal Reserve will hold its last meeting of the year, where officials are expected to cut the interest rate by 25 basis points. Recent macroeconomic data support this scenario: in September, unemployment rose to 4.4%, and the November employment report by Automatic Data Processing (ADP) showed a decrease from 47.0K to –32.0K jobs. Meanwhile, September retail sales declined from 0.6% to 0.2%, missing the forecast of 0.4%, indicating a cooling labor market and slower economic activity.

However, if today at 17:00 (GMT+2) the core Personal Consumption Expenditures (PCE) index for September remains at 2.9% or shows a reduction in inflation pressure, the likelihood of monetary easing will increase from the current 87.1%, according to the CME FedWatch Tool.

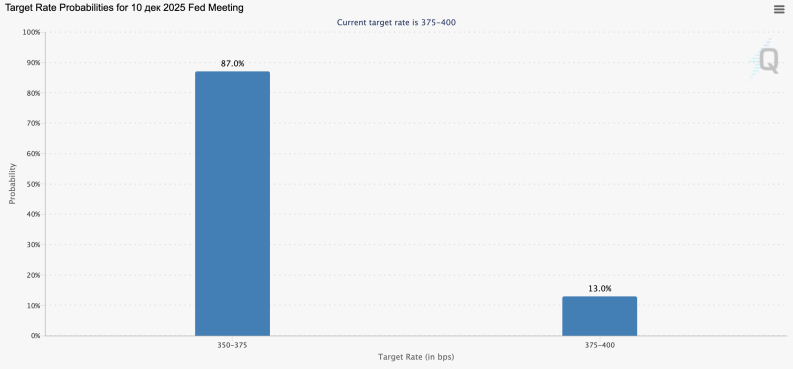

CME Group FedWatch Tool shows the probability of a 25 bps rate cut to 3.75% is above 87%.

CME Group FedWatch Tool shows the probability of a 25 bps rate cut to 3.75% is above 87%.

Eurozone

The euro is weakening against the British pound and shows mixed performance against the US dollar and the Japanese yen.

In Q3, the EU gross domestic product (GDP) accelerated from 0.1% to 0.3% quarter-over-quarter, above the forecast of 0.2%, while declining from 1.5% to 1.4% year-over-year. This confirms economic stability and reduces the need for immediate European Central Bank (ECB) support. Additionally, in October, German manufacturing orders increased by 1.5%, exceeding the expected 0.3%, mainly due to stronger demand in transport equipment such as aircraft, ships, trains, and defense products. Domestic orders rose by 9.9%, supported by government defense spending, while foreign orders declined by 4.0%.

United Kingdom

The British pound is strengthening against the US dollar, yen, and euro.

Today, Halifax Bank Plc. published housing market data: the house price index fell from 1.9% to 0.7% year-over-year, the lowest since March 2024, and from 0.5% to 0.0% month-over-month. Analysts note that investor caution is putting pressure on the market, as buyers delay expensive purchases due to expected tax adjustments in the new budget. Still, a faster recovery is projected for next year, supported by economic stabilization and further Bank of England monetary easing.

Japan

The Japanese yen is weakening against the British pound and shows mixed movement against the US dollar and euro.

Investors are evaluating household spending data: in October, spending fell to –3.5% month-over-month instead of the expected growth to 0.7%, and to –3.0% year-over-year versus 1.1%. This may ease inflationary pressure and support the Bank of Japan’s decision to keep rates unchanged in the long run. However, Governor Kazuo Ueda hinted that monetary adjustments could be discussed at the December meeting, noting that all pros and cons will be considered.

Australia

The Australian dollar is strengthening against the euro, pound, yen, and US dollar.

On Tuesday at 05:30 (GMT+2), the Reserve Bank of Australia (RBA) will hold its monetary policy meeting. With Q3 economic growth at 2.1%, strong labor market conditions (unemployment at 4.3% and employment at +42.2K in October), and inflation indicators rising to 3.3% (trimmed) and 3.4% (weighted median), the regulator is expected to keep the rate at 3.60% and delay any major adjustments until the second half of next year.

Oil

Morning weakness in oil prices was replaced by growth driven by conflicting factors. Markets continue to watch possible peace talks in the Russia–Ukraine conflict. Traders hope that successful negotiations could lead to partial sanctions relief for Russian energy companies such as Rosneft and Lukoil, increasing oil supply.

At the same time, expectations of US Federal Reserve monetary easing support commodity assets, preventing oil prices from declining more aggressively.