Forex: United States of America

October labor market data from Automatic Data Processing (ADP) showed that non-farm employment increased by 42.0K, compared to expectations of 32.0K, while August figures were revised from –32.0K to –29.0K. The strongest job growth occurred in trade (47.0K), education and healthcare (26.0K), and the financial sector (11.0K), offsetting declines in other industries. All new jobs were created by large companies with over 250 employees (76.0K), while small businesses lost 34.0K positions. Wages for those who remained in their jobs rose by 4.5% year-over-year, the same as the previous month, while employees who changed jobs saw their pay increase by 6.7%. Analysts note that this level still significantly exceeds both the current and target inflation rates, providing another argument for the Federal Reserve to maintain its current monetary policy until the end of the year.

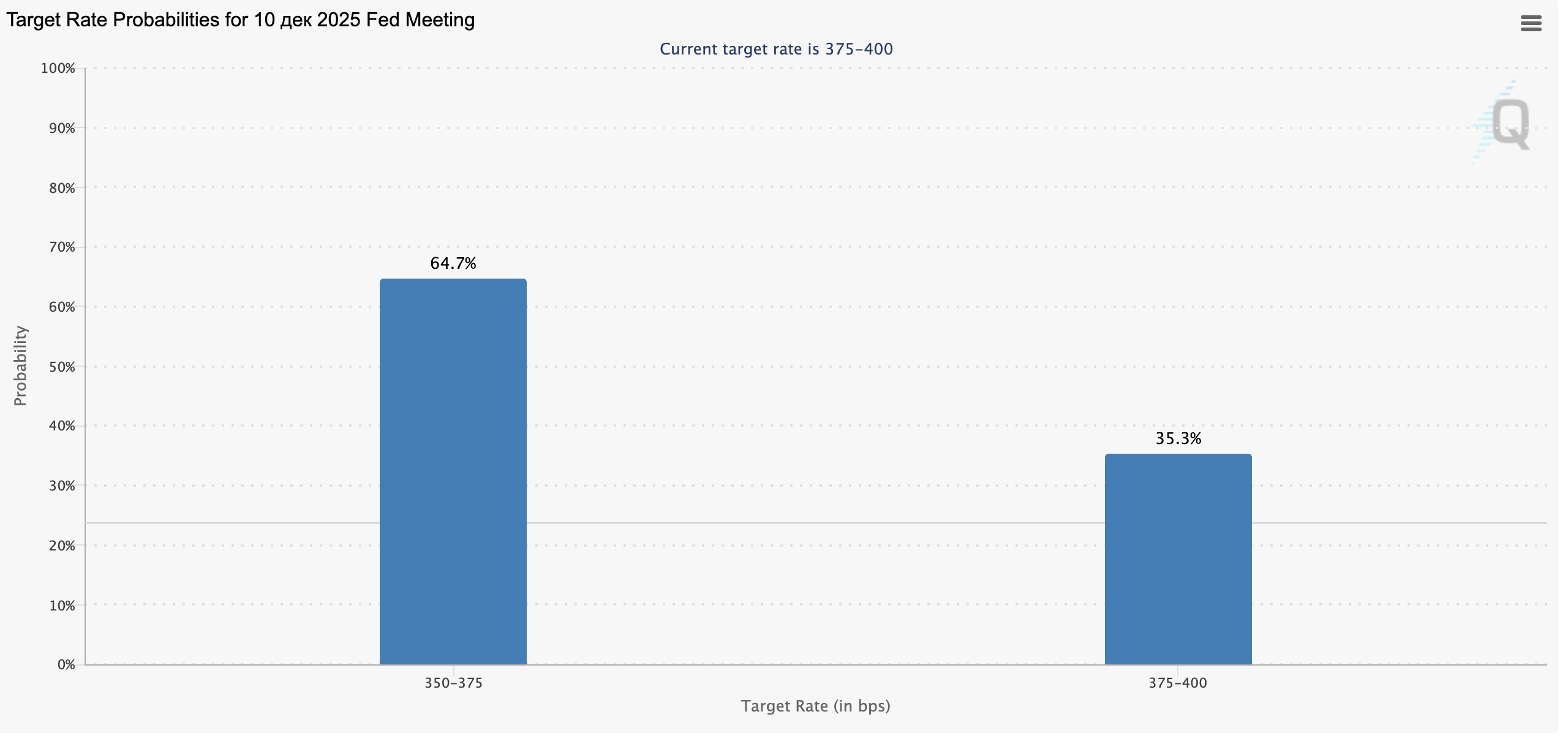

The chart shows the probabilities of changes in the Federal Funds Rate for the meeting scheduled on December 10, 2025.

Current target range: 3.75–4.00%

The market estimates two main scenarios:

- Rate cut to 3.50–3.75% — probability 64.7%

- Rate unchanged at 3.75–4.00% — probability 35.3%

Interpretation:

The majority of market participants (nearly two-thirds) expect the Federal Reserve to lower the rate by 25 basis points at the December meeting. This indicates a growing consensus in favor of a more accommodative monetary policy, likely due to slowing inflation and a cooling US economy.

If these expectations materialize, December 2025 could mark the beginning of a rate-cutting cycle, potentially supporting the stock market and gold while putting pressure on the US dollar.

Eurozone

The euro weakens against the pound and shows mixed performance against the US dollar and the yen. Investors and forex traders are assessing October activity data from EU countries: the overall services PMI for the region rose from 51.3 to 53.0 points, above the expected 52.6, while the composite index climbed from 51.2 to 52.5 versus 52.2. In Germany, the indicators improved from 51.5 to 54.6 (services) and from 52.0 to 53.9 (composite), confirming positive momentum despite ongoing trade uncertainty. In September, German factory orders increased from –0.4% to 1.1%, entering positive territory for the first time since April, signaling a possible recovery in the industrial sector. Meanwhile, the eurozone producer price index (PPI) rose from –0.4% to –0.1% month-on-month and from –0.6% to –0.2% year-on-year, remaining negative and reflecting a slowdown in wholesale inflation. Under such conditions, the European Central Bank (ECB) is unlikely to return to a dovish stance anytime soon.

United Kingdom

The pound strengthens against the euro, US dollar, and yen. October service sector data showed the PMI rising from 50.8 to 52.3 versus forecasts of 51.1, while the composite index climbed from 50.1 to 52.2 versus 51.1. This indicates that the key UK services sector continues to expand despite global trade instability. However, expectations of increased fiscal pressure in the upcoming autumn budget, estimated at 26–30 billion pounds, are limiting further currency growth. The changes may affect income and value-added taxes (VAT), putting pressure on businesses and discouraging investment and hiring.

Japan

The yen weakens against the pound and shows mixed dynamics against the US dollar and euro.

Investors and forex traders are focused on the minutes of the September Bank of Japan meeting, where the interest rate was kept at 0.50%. Most policymakers believe the conditions for tightening monetary policy are gradually forming, and two members advocated an immediate rate hike. However, given the continued rise in food prices, board members concluded that inflation expectations remain too unstable to justify a shift toward a hawkish stance.

Australia

The Australian dollar strengthens against the euro and yen but shows mixed performance in pairs with the pound and the US dollar.

October activity data showed the services PMI adjusting from 52.4 to 52.5, below preliminary estimates of 53.1, while the composite index declined from 52.4 to 52.1 versus 52.6. Although indicators remain below forecasts, the economy is not yet signaling a recession, which increases the likelihood that the Reserve Bank of Australia (RBA) will maintain its current monetary policy.

Oil

Morning oil price gains were replaced by declines as fundamentals remain unfavorable. Yesterday, the American Petroleum Institute (API) reported an increase in fuel inventories of 6.5 million barrels versus an expected drop of 2.4 million barrels. At 17:30 (GMT+2), data from the US Energy Information Administration (EIA) will be released, with forecasts indicating a decline in reserves by 2.5 million barrels, which could provide some support to oil prices.